The latest data from CreditorWatch’s Business Risk Index (BRI) has indicated that business failures are set to increase in 87.2% of regions across Australia over the next year.

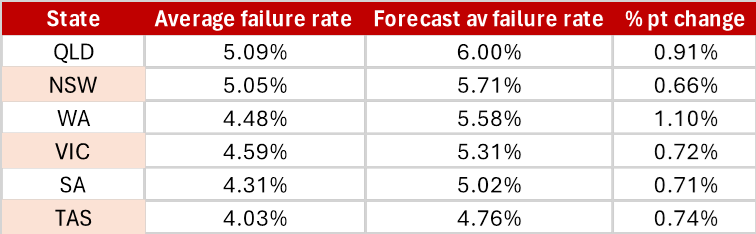

The report highlighted that Queensland is expected to face the highest rate of business failures, while Western Australia is projected to experience the largest increase in failure rates. The analysis covered 329 regions nationwide.

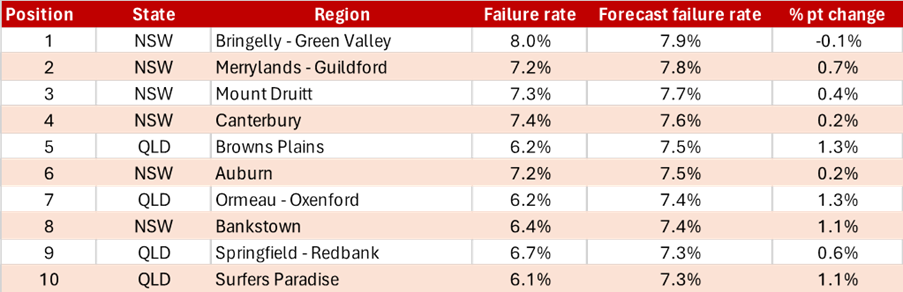

The index identified Western Sydney and South-East Queensland as high-risk areas where businesses are likely to struggle the most in the coming year. These regions are grappling with a combination of high interest rates, lower household incomes, and high commercial property prices – factors that are contributing to financial stress among local businesses.

Additionally, the ongoing rise in construction costs in Queensland is adding pressure, making it challenging to expand commercial space and alleviating rent pressures.

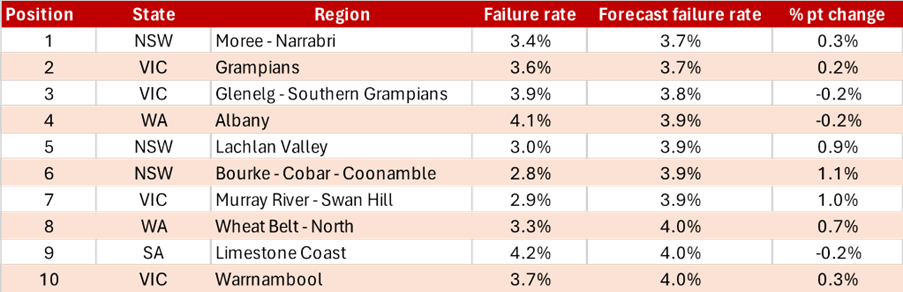

In contrast, regional areas across Australia are expected to see lower rates of business failures. These areas benefit from lower commercial rents, reduced competition, and more robust local economies, particularly in agriculture.

The agricultural sector, less affected by high interest rates due to stable demand for essential goods, continues to support these regional economies.

The report suggested that all states will see an increase in business failure rates over the next 12 months.

See LinkedIn post here.

Queensland is forecast to have the highest average failure rate at 6%, with Western Australia expected to see the most significant increase in failures. Tasmania, on the other hand, is projected to have the lowest average failure rate at 4.76%.

CreditorWatch CEO Patrick Coghlan noted that the widespread increase in business failure rates underscores the severe impact of rising interest rates, increasing costs, and declining consumer demand across Australia.

“The fact that almost 90% of regions will see an increase in the rate of business failures indicates that the current pressures from interest rates, cost increases, and declining consumer demand are being acutely felt right around the country – particularly those areas with younger populations and a higher proportion of businesses in high-risk sectors,” he said.

He expressed hope that upcoming tax cuts could help boost consumer confidence, but he warned that a substantial improvement in business conditions is unlikely until the Reserve Bank of Australia (RBA) begins to cut interest rates.

Anneke Thompson, chief economist at CreditorWatch, added that consumer confidence remains low, despite some minor improvements reported in recent surveys.

“While consumers are now less fearful of an increase in interest rates, and also report a small positive sentiment increase from tax cuts, the increase in confidence is not nearly enough to suggest that household consumption will recover any time soon,” she said.

She highlighted that declining household spending is likely to continue to weigh on businesses, particularly those in sectors sensitive to discretionary spending.

The report also noted a sharp decline in business orders, with the average value of invoices dropping by 51.5% year-on-year as of July 2024. This significant decrease reflects the broader slowdown in consumer demand and stagnant retail trade.

In addition, legal actions against businesses have surged beyond pre-pandemic levels as creditors increasingly pursue debt recovery. This rise in court actions suggests that many businesses are struggling to meet their financial obligations, particularly in the face of rising costs and declining revenues.

CreditorWatch anticipates that the difficult conditions facing Australian businesses will persist until at least the first quarter of 2025, when the RBA may consider lowering the cash rate. The economic pressures are expected to hit regions with younger populations and sectors reliant on discretionary spending particularly hard.

Despite the challenges businesses are facing, the RBA is unlikely to reduce interest rates in the near future.

Recent data showing a 4.1% annual increase in the Wage Price Index and an improvement in consumer sentiment suggest that price pressures remain in the economy, making it difficult for the central bank to ease monetary policy at this stage.