A recent nationwide survey has found that a substantial portion of Australians remain unclear about the insurance held within their superannuation accounts, raising concerns about transparency and engagement within the system.

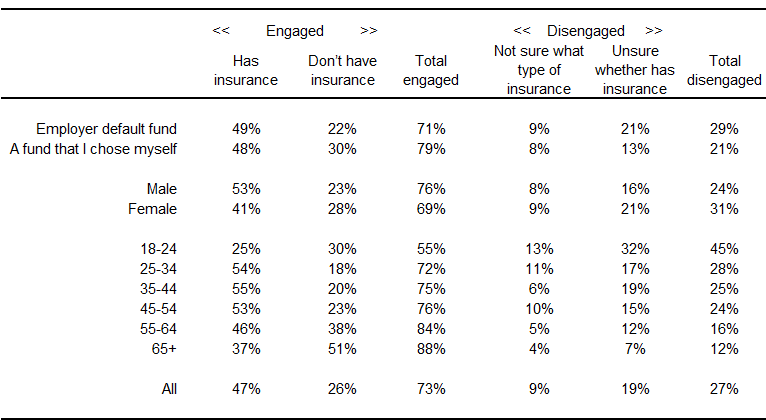

According to data released by Super Consumers Australia as part of its 2024 Pulse survey, 27% of Australians either do not know if they have insurance through their super fund (19%) or are unsure about the details of the coverage they are paying for (9%).

The 2024 Pulse survey was conducted May 14-24, with responses collected from a representative sample of Australians aged 18 to 75. The research was supported by the Ecstra Foundation, a philanthropic group focused on improving financial well-being.

The survey of over 1,500 adults found that awareness is particularly low among young adults. Nearly half of respondents aged 18-24 were unaware of their insurance status, a group typically not covered by default insurance until they turn 25.

Among those aged 25-29 – most of whom would have recently been enrolled in default cover – more than half did not know this automatic enrolment takes place or incorrectly believed it did not.

Despite super funds collectively receiving over $6.7 billion in premiums for group insurance in the 2023-24 financial year, understanding of these products remains limited. These default policies often include life, total and permanent disability (TPD), and income protection cover, but are not tailored to individual circumstances.

Super Consumers Australia is calling for a review by the Productivity Commission to evaluate whether the current model of providing insurance through super meets the needs of members.

The organisation is also recommending that super funds improve engagement at key transition points – such as the age when default insurance begins – to help members make informed decisions.

The survey identified several patterns:

The findings come on top of the Australian Securities and Investments Commission’s (ASIC) warning that many super trustees are not adequately prepared to address the growing risk of scams targeting fund members. In a recent review of 15 trustees, ASIC found that none had implemented an organisation-wide anti-scam strategy.

ASIC Commissioner Simone Constant noted that as more Australians reach preservation age, they become more exposed to scams due to higher account balances and fewer withdrawal restrictions.

“Over the coming decade, an increasing number of superannuation fund members will reach preservation age. While all members are vulnerable to scams and fraud, members who have reached preservation age face fewer frictions in accessing their funds and tend to have higher account balances. These factors can make them attractive targets,” she said.

Super Consumers Australia also cited previous findings from the Productivity Commission showing that insurance premiums can significantly erode retirement savings.

For example, a low-income worker in a hazardous occupation may lose up to $125,000 from their retirement balance due to group insurance costs.

The organisation is calling for a broad inquiry into the appropriateness and efficiency of insurance in superannuation, including whether it duplicates or overlaps with other government support systems like workers’ compensation, the National Disability Insurance Scheme, or Centrelink payments. Alternative approaches, such as New Zealand’s no-fault accident compensation model, should also be considered, it said.

As debate over the role of insurance in superannuation intensifies, the Council of Australian Life Insurers (CALI) has committed to working with the federal government on new initiatives aimed at improving member outcomes.

“Life insurance works hand in hand with super to protect people’s nest eggs and allow them to have a dignified and financially secure retirement if they can’t live a full working life,” said CALI CEO Christine Cupitt.