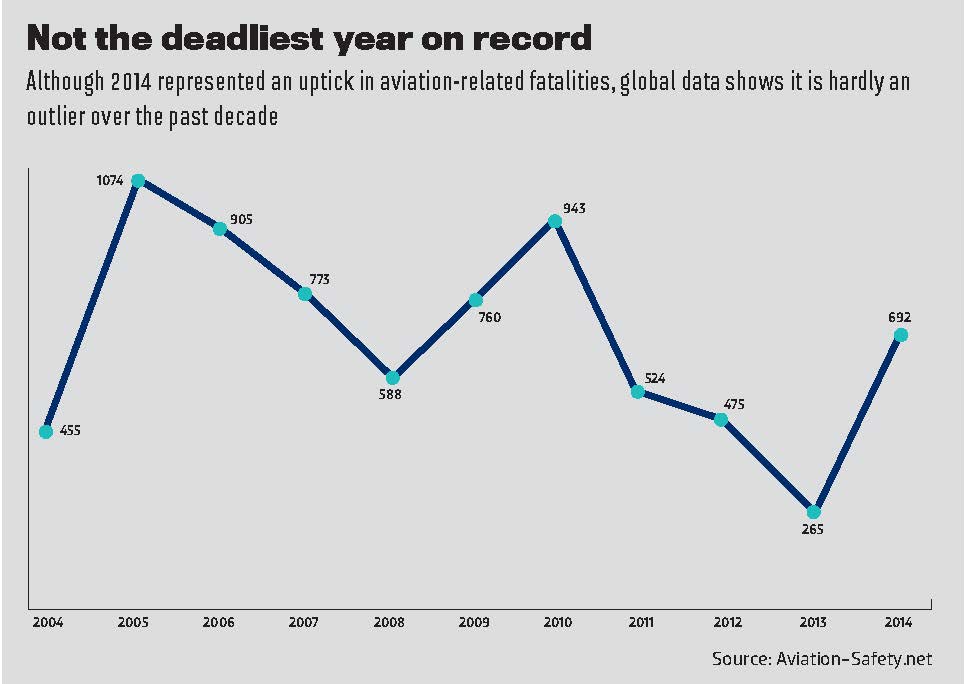

Since Early 2014, the world has witnessed some of the highest profile air disasters it’s seen for some time.

It was 8 March of last year when Malaysia Airlines flight MH370 vanished from radar, presumed to have crashed into the southern Indian Ocean. There were 239 people on board.

Barely four months later, on 17 July, Malaysia Airlines lost another aircraft. This time, flight MH17 was shot down by a missile over the Ukraine, killing all 283 passengers and 15 crew members.

In December, Air Asia Flight QZ8501 crashed into the Java Sea, the cause believed to have been bad weather. It claimed the lives of 162 people travelling from Surabaya in Indonesia to Singapore.

And earlier this year in March, Germanwings Flight 4U9525 flew into a mountain in the French Alps, and all 150 people on board lost their lives. Investigators believe the co-pilot, Andreas Lubitz, intentionally flew the plane into the mountain.

Despite the scale of recent disasters that have made global headlines, the impact on the aviation insurance market has been unremarkable. According to Daniel B Crispe, the head of aerospace for

AIG in the Asia-Pacific region, “there have definitely been signs of the market hardening during Q4 [2014], which is when the majority of airlines renewals fall due, however, there is so much capacity currently in the aviation sector that the impact hasn’t been as significant as many would have expected.”

Robert Phillips, manager of aerospace at

JLT Australia, offers a similar assessment. “Now that the dust has settled on 2014, insurers have had the opportunity to fully digest the events of last year,” he says. “The consensus of opinion is that these losses, in their own right, will not create a definitive hardening of market conditions for 2015.”

But he also says that the recent major loss in Quarter 1, 2015 will “no doubt create an immediate sense of market fragility.”

Scott Guse, an audit partner for

KPMG Australia in the insurance field, says most airlines renew their policies either 1 October or 1 November each year, and so both of the Malaysia Airlines events would have been factored into prices set for the most recent renewal period. He says, “what we saw in the most recent round of insurance renewals… was that most airlines received pretty much a premium consistent with last year. There were obviously a couple that had significant increases. Malaysia [Airlines] would have obviously been one of them… but the majority…were pretty much flat with their premiums.

“If you were going to see an increase in the premiums, you would have certainly seen it in this most recent renewal period…”

Aerial view

Guse says that high profile crashes such as those seen in recent times account for, on average, a quarter of insurance claims that come from the aviation industry. “There are an enormous number of minor incidents that really add up to a lot of dollars for insurance companies,” he says. “It’s little incidents such as planes over-shooting runways, plane wings clipping other plane wings on the tarmac, planes running into aerobridges, and even baggage handler carts running into plane wheels…”

Phillips says that as tragic as the events of 2014 were, the situation could have been far worse from a financial loss perspective, pointing to the opinion of many experts as to how differently things could have played out if those major accidents had occurred in a more litigious environment. Guse also raises the dramatically different values that courts around the world place on human life. “If a lawyer launched a litigation suit against Malaysia Airlines, it would be heard in a Malaysian court. The chances are that passengers that died in those flights would be compensated in the vicinity of $100,000 per passenger.

“If you had a Delta [Air Lines] flight that flew off from New York and crashed somewhere in the US and everyone on board died, you’d have litigation lawyers in the court asking for at least $5m per person and, more often than not, they would get that.

“So while the Malaysia Airlines incidents are very high profile, the actual [financial] cost to the industry… is not as great as it would have been had they happened inside the US, and [the cost] would have been tenfold probably if they happened inside the US.”

According to Guse, it would take “something like a 9/11” to cause step change in the cost of insurance for airlines. Phillips says, “I guess the point to be stressed is that the aviation insurance industry is one which has always needed to respond to the unexpected catastrophic perils thrown at it, and the challenges faced today are certainly not unique in this regard.”

The marketplace

Of course, the wealth of competition in the market is another big part of the story. “There are a lot of players in the insurance field that want a piece of the action because it’s seen as a glamorous product, a product they should have in their suite of offerings if they really want to be a global, holistic insurer,” Guse says. “It is very competitive and, at the moment, there is an enormous amount of capacity wanting a piece of most insurance markets, including aviation.

“The reason there’s a lot of capacity is that… a lot of venture capitalists and high net worth individuals essentially want greater return for their money and so they’re willing to take on greater risks, and aviation insurance has seen an influx of venture capitalists come into being a form of insurance protection for those airlines.”

While a significant hardening of the market hasn’t resulted from recent events, cautiousness on the part of airlines may increase, and we may see greater efforts than ever before focused on risk mitigation. Describing the climate following events in this first quarter as “a lot more fragile”, Phillips says insurers will be counting the cost of those losses and reviewing their risks more closely.

Safety first

When it comes to safety in the aviation space, the most recent events have prompted a great deal of discussion around cockpit and cabin security. It seems fair to conclude that discussion will be ongoing for many months to come.

Crispe says aircraft manufacturers, airlines and regulators are constantly striving to improve safety in an industry already renowned for offering the safest form of transportation. He says that we’ll inevitably see more innovation in the space in the coming years, “whether it be mandating of aircraft tracking, locating systems or more advanced systems for weather monitoring…”

Crispe tells Insurance Business that Airbus has developed a system intended to reduce or prevent overruns. Overruns can have potentially catastrophic consequences, including property damage and loss of life.

He expects to see players in the market put “more focus on risk selection, business mix and analytics to ensure that the business remains sustainable in years to come.”

Guse says reputational impact from air crashes will change and drive better risk mitigation steps. He sees most airlines reconsidering flight paths and destinations and while he can’t foresee climate change prompting any major changes at this point in time, he says it, too, is an issue very much on the radar screens of airlines.

But the biggest threat to the airline industry nowadays, according to Guse, comes from cyber-attacks. “Everything is automated on planes and, if someone can get control of a plane remotely through computers, it’s very hard to counteract that. Cyber threats are certainly high on the aviation industry radar.”

However, Guse sees the cyber threat offering opportunities to those in the aviation insurance market. “Trying to factor in pricing to cyber threats in aviation policies is certainly a bit of a black box at the moment. No one really knows how you can do it. But there are a number of companies that are exploring the cost of cyber risks and how much should be factored into premiums.”

While commentators can use their expert knowledge to try and predict the skies ahead, Phillips offers an important reminder: “Last year taught us that you cannot make clear and accurate market predictions in the wake of a significant market loss.”