Financial conditions in the U.S. insurance market

As 2024 unfolds, the U.S. insurance sector is showing resilience, with the top 20 insurers by market capitalization reporting strong profitability in the first three quarters of the year. This report highlights key trends shaping the industry and takeaways for insurers and brokers alike.

This analysis offers an early look at market conditions ahead of our full report, set for release in March. That comprehensive edition will include Q4 data and an expanded view of the top 85 U.S. insurers by market cap. To receive it as soon as it's published, sign up here.

A strong year for P&C insurers

The property and casualty (P&C) sector posted robust gains in 2024, driven by premium growth, improved underwriting results, and rising investment income.

As insurers navigate an evolving landscape, these financial trends underscore a market that is adapting—and thriving—amid changing economic conditions.

By contrast, the health insurance sector faced mounting pressures in 2024, as escalating healthcare costs and tighter reimbursement rates in government programs weighed on profitability.

Even as health insurers posted strong revenue growth, rising medical costs and deteriorating margins underscored the challenges ahead—especially for those reliant on government-backed plans.

Key trends shaping the insurance market

The 2024 market landscape ushered in several pivotal trends that reshaped the strategies of insurers and brokers alike.

Insurers across sectors accelerated their adoption of digital technologies to enhance efficiency, cut costs, and improve customer experience. In the P&C sector, companies like Progressive leveraged AI-driven claims processing and automated underwriting to sharpen their competitive edge and manage risk exposure more effectively.

Insurers with sizable investment portfolios—including MetLife and Prudential—faced headwinds as equity market volatility and shifting interest rates weighed on returns. Life insurers, in particular, struggled with lower-than-expected yields from fixed-income assets, prompting a strategic pivot toward alternative investments such as real estate and infrastructure.

As cyberattacks and data breaches surged, demand for cyber insurance climbed. Insurers such as AIG, Chubb, and The Hartford expanded their offerings in response. Yet, pricing and claims challenges intensified, as insurers grappled with the evolving nature of cyber risks and the growing complexity of underwriting in this space.

The increasing frequency of natural disasters forced insurers to reassess their pricing strategies, particularly in high-risk regions such as flood zones and coastal areas. Companies like Cincinnati Financial and The Travelers Companies refined their underwriting models and claims management processes to adapt to escalating climate-related risks.

As the industry moves forward, underwriting profitability, cost containment, and regulatory navigation will be critical to success. Brokers would do well to align with insurers that prioritize operational efficiency, digital innovation, and proactive risk management—essentials for staying competitive in an evolving market.

Profit shifts in 2024

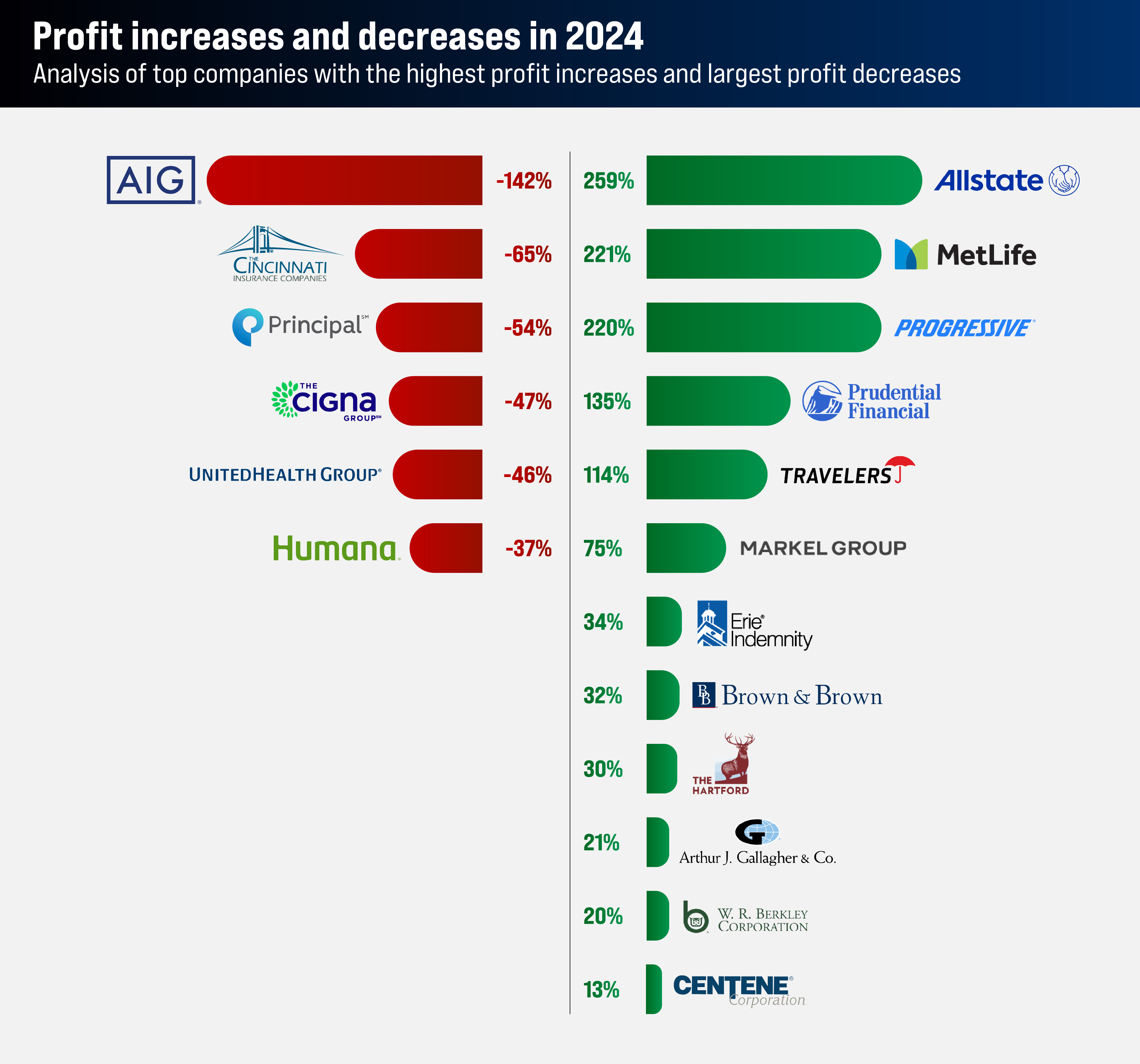

The first three quarters of 2024 brought significant profit fluctuations across the U.S. insurance market, reflecting a mix of sector-specific challenges and strategic successes. While some insurers capitalized on favorable conditions to post strong gains, others saw profits eroded by rising costs and shifting market dynamics.

This section examines the five companies that recorded the most substantial profit increases—and the five that faced the steepest declines—along with the key factors behind these movements.

Companies with the highest profit increases

1. The Allstate Corporation

Allstate emerged as one of the standout performers in the U.S. insurance market during the first three quarters of 2024, posting a dramatic 259% increase in profits. The company rebounded from a modest $4 million loss in Q3 2023 to a striking $1.164 billion profit by Q3 2024, signaling a robust recovery. This turnaround was largely attributed to enhanced claims management, which allowed Allstate to reduce claims payouts and optimize operational costs. Additionally, rate hikes in auto and homeowners’ insurance boosted profitability, while a surge in weather-related claims—driven by natural disasters—increased demand for coverage. Despite facing rising catastrophe losses and higher advertising expenses, Allstate's focus on cost control and improved risk management played a crucial role in its strong profit growth.

For the first nine months of 2024, Allstate’s performance was equally impressive, with a 14.7% increase in revenue and net income of $1.2 billion.

Financial highlights:

Factors driving profit growth:

Challenges impacting profit growth:

Despite the overall positive performance, several challenges affected Allstate's profitability in Q3 2024:

While Allstate navigated these challenges effectively, its strategic focus on premium rate adjustments, operational efficiencies, and claims management helped fuel impressive profit growth, setting the stage for continued success in the evolving insurance landscape.

2. MetLife

MetLife reported a 221% increase in profits over the first three quarters of 2024, with Q3 profits soaring to $1.341 billion—up from $495 million in the same period a year earlier. This impressive jump was driven by strong sales in the company’s life insurance and retirement solutions segments, which fueled both revenue and profit growth. In addition, MetLife benefited from a surge in investment income, propelled by favorable market conditions and effective investment management strategies. Cost optimization in its employee benefits and group insurance divisions also contributed to the company’s robust performance.

Key financials

Contributors to profit growth

Challenges to profit growth

Despite strong profits, MetLife faced several hurdles:

MetLife's ability to navigate these challenges while delivering substantial profit growth underscores its strong position in the market—but also highlights the ongoing risks in a volatile economic environment.

3. The Progressive Corporation

Progressive saw a remarkable 220% increase in profits from the first three quarters of 2023 to the same period in 2024, with Q3 2024 profits reaching $2.33 billion, up from $1.12 billion in Q3 2023. This impressive growth was driven by a 25% rise in net premiums written, fueled by strong demand for its personal auto insurance products. Progressive’s focus on operational efficiency, particularly through automated claims processing and data-driven underwriting, helped reduce costs and improve profit margins. Additionally, premium rate hikes further supported its profit expansion.

Financial highlights

Factors driving profit growth

Challenges to profitability

Despite these challenges, Progressive’s operational efficiency and premium growth contributed to one of the strongest profit performances in the insurance sector for 2024.

4. Prudential Financial

Prudential Financial staged a remarkable recovery in 2024, increasing its profit by 135% from the first three quarters of 2023. The company reversed a loss in Q3 2023, posting a profit of $451 million in Q3 2024, compared to a $791 million loss a year earlier. This impressive turnaround was driven by strong sales in life insurance and retirement products, as well as better-than-expected investment performance. Prudential also benefited from cost management improvements, particularly in its pension funds and asset management divisions.

Financial highlights

Key Drivers of Profit Growth

Challenges to profit growth

5. The Travelers Companies

The Travelers Companies reported a 114% increase in profits for the first three quarters of 2024, with Q3 profits rising to $1.26 billion, up from $404 million in Q3 2023. This remarkable growth was driven by strong underwriting results in its commercial property and casualty insurance businesses. Travelers' ability to effectively manage claims and improve its loss ratio played a central role in its performance. Additionally, growth in both personal lines and commercial insurance boosted premiums and profits, while cost control measures helped keep administrative expenses low.

Financial highlights

Key drivers of profit growth

Challenges to profitability

These companies capitalized on a blend of robust market demand, enhanced claims management, premium rate increases, and operational efficiencies. They underscore the critical role of underwriting profitability, cost control, and savvy investment strategies as central drivers of profit growth. For brokers and insurers, these firms present compelling partnership opportunities, especially in the realms of auto insurance, life insurance, retirement solutions, and property/casualty coverage.

Companies with the largest profit decreases

1. American International Group

American International Group (AIG) experienced a dramatic 142% decline in profits, plunging from $2.747 billion in Q3 2023 to just $457 million in Q3 2024. The company’s diversified portfolio in commercial insurance and property was severely impacted by global market volatility and rising claims, particularly in its property and casualty segments. Operational costs also increased, and the company struggled to improve its claims ratios. AIG's performance highlights the vulnerability of insurers to global economic shifts and underscores the importance of effective claims management and cost control in navigating these turbulent conditions.

Revenue: AIG reported net premiums written of $6.4 billion for General Insurance in Q3 2024, a 1% decrease on a reported basis, though a 6% increase on a comparable basis. The global commercial lines segment saw a 7% rise in net premiums written, driven largely by strong growth in North America, where Commercial Lines grew by 11%.

Profit: AIG posted net income of $459 million, or $0.71 per diluted share, for Q3 2024, a sharp drop from $2.0 billion, or $2.81 per diluted share, a year earlier. The decrease was mainly attributed to a reduction in income from discontinued operations following the deconsolidation of Corebridge. However, adjusted after-tax income stood at $798 million, or $1.23 per diluted share, reflecting a solid 18% increase from the prior year.

Combined ratio: The combined ratio for Q3 2024 was 92.6%, a solid outcome that reflected strong underwriting results. The accident year combined ratio, adjusted for catastrophe losses, improved to 88.3%.

Return on Equity: AIG’s return on equity (ROE) for Q3 2024 was 4.1%, down significantly from 19.8% in the same period last year.

Factors driving profit growth

Commercial lines growth: AIG’s global commercial lines segment saw a 7% increase in net premiums written, with particularly robust performance in North America, which grew by 11%. The company also achieved $1.1 billion in new business written, marking a 9% year-over-year increase.

Underwriting results: The adjusted accident year combined ratio improved to 88.3%, driven by strong underwriting results in global commercial lines, despite the challenges posed by catastrophic events. The company’s ability to maintain an 88% retention rate in commercial lines further supported its underwriting profitability.

Investment income: AIG saw a 14% increase in net investment income for Q3 2024, reaching $973 million, fueled by higher returns from alternative investments, equities, and fixed maturity securities. General Insurance also saw an 8% increase in net investment income on a comparable basis.

Capital management: AIG returned $1.8 billion to shareholders in Q3 2024, including $1.5 billion in stock repurchases and $254 million in dividends. These capital returns were made possible by the company’s strong capital position and disciplined capital management.

Challenges to profit growth

Catastrophe losses: AIG faced $417 million in catastrophe-related charges during Q3 2024, stemming from events such as Hurricane Helene and severe wind and hailstorms. These catastrophe events added 6.9 points to the combined ratio, pressuring profitability. However, the company’s overall underwriting performance remained resilient despite these challenges.

Discontinued operations impact: A substantial portion of the year-over-year decline in net income was linked to the deconsolidation of Corebridge, which reduced AIG’s income from discontinued operations. While strong core earnings partially offset this, the reduction in income from these operations remained a challenge for the quarter.

2. Cincinnati Financial Corporation

Cincinnati Financial Corporation experienced a dramatic 65% decline in profits in 2024, but managed a strong recovery in the third quarter, posting profits of $820 million—up from a $99 million loss in the same period the previous year. While the company rebounded in Q3, its overall performance was still impacted by the significant risks tied to weather-related claims, a persistent concern for insurers with high exposure to property risks. The combination of adverse weather events, underwriting challenges, and potential investment losses contributed to the profit decline. For brokers, Cincinnati Financial underscores the importance of solid underwriting practices and risk diversification in managing the financial impacts of weather-related claims.

Cincinnati Financial's performance in Q3 2024 highlights the challenges and opportunities faced by insurers with significant property exposure. While catastrophe losses have pressured profitability, the company’s strong underwriting discipline and investment gains helped fuel its recovery, positioning it well for future growth despite ongoing market uncertainties.

3. Principal Financial Group

Principal Financial Group saw a dramatic 54% decline in profits for Q3 2024, posting a loss of $193 million, compared to a $1.25 billion profit during the same period in 2023. The company’s struggles stemmed primarily from a sharp decline in investment income, a key driver for its retirement solutions and life insurance segments. Additionally, regulatory pressures related to pension funds and retirement planning further compressed margins. Principal’s performance highlights the vulnerability of insurers heavily reliant on investment income, underscoring the need for more diversified revenue streams to weather market volatility.

Revenue: Principal Financial reported a net loss attributable to the company of $220 million, or $0.95 per diluted share for Q3 2024. This loss was largely attributed to the exit of certain business segments. However, excluding these exited segments, the company posted non-GAAP net income of $419 million, or $1.78 per diluted share, driven by strong performance in its core business.

Profit: Non-GAAP operating earnings for the quarter totaled $412 million, or $1.76 per diluted share, while adjusting for significant variances, the company recorded $480 million in operating earnings, or $2.05 per share.

Assets Under Management (AUM): Principal reported AUM of $741 billion and $1.7 trillion in assets under administration, reflecting solid growth across its investment and retirement solutions segments.

Factors contributing to profit growth

Retirement and income solutions: Principal’s retirement and income solutions segment demonstrated a 40% operating margin, excluding significant variances, and achieved 10% recurring deposit growth. This performance underscores strong demand in the retirement sector, coupled with effective management of retirement solutions.

Principal Global Investors (PGI): Principal’s PGI segment managed $541 billion in AUM, an increase of $28 billion from Q2 2024 and $72 billion from Q3 2023. This growth was fueled by solid investment returns and inflows from clients.

Principal international: The company’s international business posted record pre-tax operating earnings of $121 million and set a new record for AUM at $185 billion. The segment also saw robust net cash flow of $2.3 billion, including $2.1 billion from investment management.

Life insurance: Principal’s life insurance segment grew market premiums and fees by 12% compared to the previous year, driven by strong demand for life insurance products.

Factors challenging profit growth

Exit of business: The $220 million net loss was primarily driven by the company’s exit from certain business segments, impacting overall profitability. While this loss was significant, it was confined to the exited businesses, and the company continued to report strong results in its core operations.

Market volatility and catastrophe losses: Although not detailed specifically, the company’s performance was likely influenced by broader market volatility. This could have included challenges within certain investment portfolios amid rising interest rates and fluctuations in the equity market, potentially impacting asset performance across several of Principal’s segments.

4. The Cigna Group

Cigna posted a 47% decrease in profits for Q3 2024, with earnings falling to $825 million, down from $1.449 billion in Q3 2023. The company’s decline was largely driven by healthcare cost inflation, which resulted in higher-than-expected claims. Additionally, its Medicare Advantage segment faced rising enrollment costs, while navigating complex regulatory changes further pressured profitability. Cigna’s struggles reflect broader challenges confronting health insurers, as they contend with escalating medical costs and a volatile regulatory environment.

Revenue: Cigna reported total revenue of $63.7 billion for Q3 2024, a 30% increase from the same period in 2023. This growth was mainly driven by robust contributions from Evernorth Health Services, which saw strong specialty volume growth and secured several large client wins.

Profit: The company posted net income of $825 million, or $2.63 per share, for Q3 2024, a sharp decline from $1.4 billion, or $4.74 per share, in Q3 2023. The drop in profit was primarily attributed to a non-cash after-tax investment loss of $1.0 billion, or $3.69 per share, linked to VillageMD. However, adjusted income from operations for Q3 2024 was $2.1 billion, or $7.51 per share, reflecting solid performance in its health services segment.

Adjusted income from operations: Cigna’s adjusted income from operations increased 5% compared to Q3 2023, driven by strong performance in Evernorth Health Services, particularly in its Specialty and Care Services divisions.

Factors contributing to profit growth

Evernorth Health Services: The growth of Evernorth Health Services played a pivotal role in the company’s profitability, buoyed by large client wins and increased specialty volume. This segment, which encompasses specialty and care services, contributed significantly to adjusted income.

Revenue growth: Cigna’s 30% revenue increase was largely attributed to Evernorth’s performance, underscoring the company’s success in executing its strategic plan within the competitive health services market.

Operational efficiency: The company’s SG&A expense ratio dropped to 5.6% in Q3 2024, down from 7.7% in Q3 2023, reflecting strong revenue growth and effective cost management. Additionally, the adjusted SG&A expense ratio improved to 5.5%, from 7.3% a year earlier, further highlighting Cigna’s operational efficiency.

Factors challenging profit growth

Investment losses: Cigna’s financial results were significantly impacted by a non-cash after-tax investment loss of $1.0 billion, or $3.69 per share, stemming from its VillageMD investment. While substantial, the loss was a one-time event, and the company’s core business segments continued to perform well.

Lower net investment income: Net investment income fell in Q3 2024 compared to the previous year, partially offsetting the strong operating income generated by Evernorth Health Services. This decline reflects broader market conditions that have affected investment performance.

5. UnitedHealth Group Incorporated

Despite continuing robust revenue growth, UnitedHealth reported a 46% drop in profits for Q3 2024, with earnings rising to $6.258 billion, compared to $6.038 billion in the same period last year. The decline in profitability was largely driven by heightened healthcare utilization, rising medical costs, and a backlog of delayed medical procedures due to the pandemic. Additionally, cybersecurity costs, particularly from its subsidiary Change Healthcare, added to operational expenses. UnitedHealth’s results underscore the mounting challenges facing health insurers, which are grappling with both rising healthcare costs and the increasing threat of cyberattacks.

These struggles echo a broader trend among health insurers such as AIG and Cigna, which also experienced profit declines driven by market volatility, higher claims, operational inefficiencies, and investment underperformance. For brokers, these companies exemplify the risks inherent in partnering with firms exposed to global economic fluctuations, healthcare cost inflation, and sector-specific vulnerabilities such as weather-related risks and cybersecurity threats.

Revenue: UnitedHealth reported total revenues of $100.8 billion for Q3 2024, marking an $8.5 billion increase year-over-year. The growth was largely fueled by significant expansion in the number of individuals served by its Optum and UnitedHealthcare divisions, with particular strength in commercial and state-based community offerings.

Profit: The company reported earnings of $6.51 per share for Q3 2024, reflecting solid performance despite the impacts of a cyberattack. Adjusted earnings, excluding business disruption and cyberattack response costs, were $7.15 per share, highlighting strong growth across both its health services and insurance segments.

Medical care ratio: UnitedHealth’s medical care ratio for Q3 2024 increased to 85.2%, up from 82.3% in Q3 2023. This rise was primarily driven by reductions in CMS Medicare funding, medical reserve adjustments, and shifts in business and member mix. Despite these challenges, the company effectively managed its medical costs.

Return on equity: UnitedHealth delivered a return on equity of 26.3% for Q3 2024, underscoring its ability to generate substantial returns on capital. This strong performance is a testament to the company’s consistent earnings and efficient capital management.

Factors contributing to profit growth

Strong expansion in health services: The company’s growth was significantly driven by strong performances across both Optum and UnitedHealthcare. UnitedHealthcare alone saw a 5% increase in revenues, reaching $74.9 billion, with notable growth in its commercial offerings and state-based community programs.

Growth in consumers served: Year-to-date, UnitedHealthcare expanded its customer base by 2.4 million, reaching a total of 29.7 million consumers. This expansion highlights the strength of the company’s consumer-focused product offerings and growing demand for its services.

Strong medicare advantage offering: UnitedHealthcare continues to experience strong growth in its Medicare Advantage segment, now serving 9.4 million seniors and individuals with complex health needs. The company’s 2025 Medicare Advantage plans are set to reach 96% of eligible Medicare beneficiaries, contributing significantly to its overall growth.

Operational efficiency: UnitedHealth’s operating cost ratio improved to 13.2% in Q3 2024, down from 15.0% in the prior year. This improvement reflects the company’s ongoing focus on cost management while maintaining growth across its business segments.

Factors challenging profit growth

Cyberattack and business disruptions: The company faced an unfavorable impact of $0.3 billion on earnings due to a cyberattack. Additionally, disruptions in services provided by Change Healthcare contributed another $0.12 per share in negative impacts to adjusted earnings, further eroding profitability for the quarter.

Increased medical care ratio: The company’s medical care ratio rose to 85.2%, driven by CMS Medicare funding reductions and changes in its business and member mix. While still within an acceptable range, this increase puts additional pressure on managing medical care costs.

Conclusion

Insurers experiencing the most significant profit gains have largely capitalized on strong market demand, operational efficiencies, and effective claims management, particularly in the property and casualty (P&C), life insurance, and retirement solutions sectors. Conversely, those facing the sharpest profit declines have been weighed down by external challenges, including global economic volatility, healthcare cost inflation, and cybersecurity risks.

Among the five insurers with the greatest profit increases, all saw substantial revenue growth driven by premium hikes and strong underwriting performance. Companies like Allstate, Progressive, and Travelers benefitted from rising rates and sustained demand for property casualty insurance. Robust investment income also helped many of these firms—especially MetLife, Progressive, and Travelers—maintain profitability, even in the face of significant challenges such as catastrophe losses, a common theme for the quarter. Still, prudent capital management and disciplined underwriting practices played key roles in mitigating the impact of such setbacks.

On the flip side, the five insurers with the most considerable profit declines shared a common thread: strong premium growth and investment performance helped offset substantial underwriting challenges, particularly those stemming from catastrophic events, medical cost inflation, and cybersecurity risks. While these companies posted strong results in their core segments, weather-related risks and escalating medical expenses continue to weigh heavily on their profitability. Despite this, capital management remained a strong suit for many, with Cigna and AIG delivering notable returns to shareholders, underscoring their commitment to efficiency and value. Yet, ongoing cybersecurity threats and regulatory challenges suggest that these issues will continue to shape their financial outlook in the near future.

Key challenges for the most affected insurers include catastrophe losses and rising healthcare costs. AIG, Cincinnati Financial, and UnitedHealth all faced significant hurdles from catastrophe-related claims. AIG incurred $417 million in catastrophe charges, while Cincinnati's combined ratio spiked by 13 points due to Hurricane Helene. These unforeseen events took a heavy toll, particularly for companies with high exposure to property claims. Meanwhile, Cigna and UnitedHealth struggled with increasing healthcare costs, with Cigna seeing rising Medicare Advantage enrollment costs and escalating medical claims. UnitedHealth's medical care ratio climbed to 85.2%, driven by Medicare funding cuts and shifts in member mix, reflecting broader challenges within the health insurance sector.

For brokers and insurers, these insights emphasize the importance of strong underwriting, cost-containment strategies, and operational flexibility in navigating both profit growth and declines. Carefully assessing risk exposure—particularly in areas like property claims, healthcare costs, and cybersecurity—will be crucial as insurers and brokers contend with the evolving market conditions of 2024.

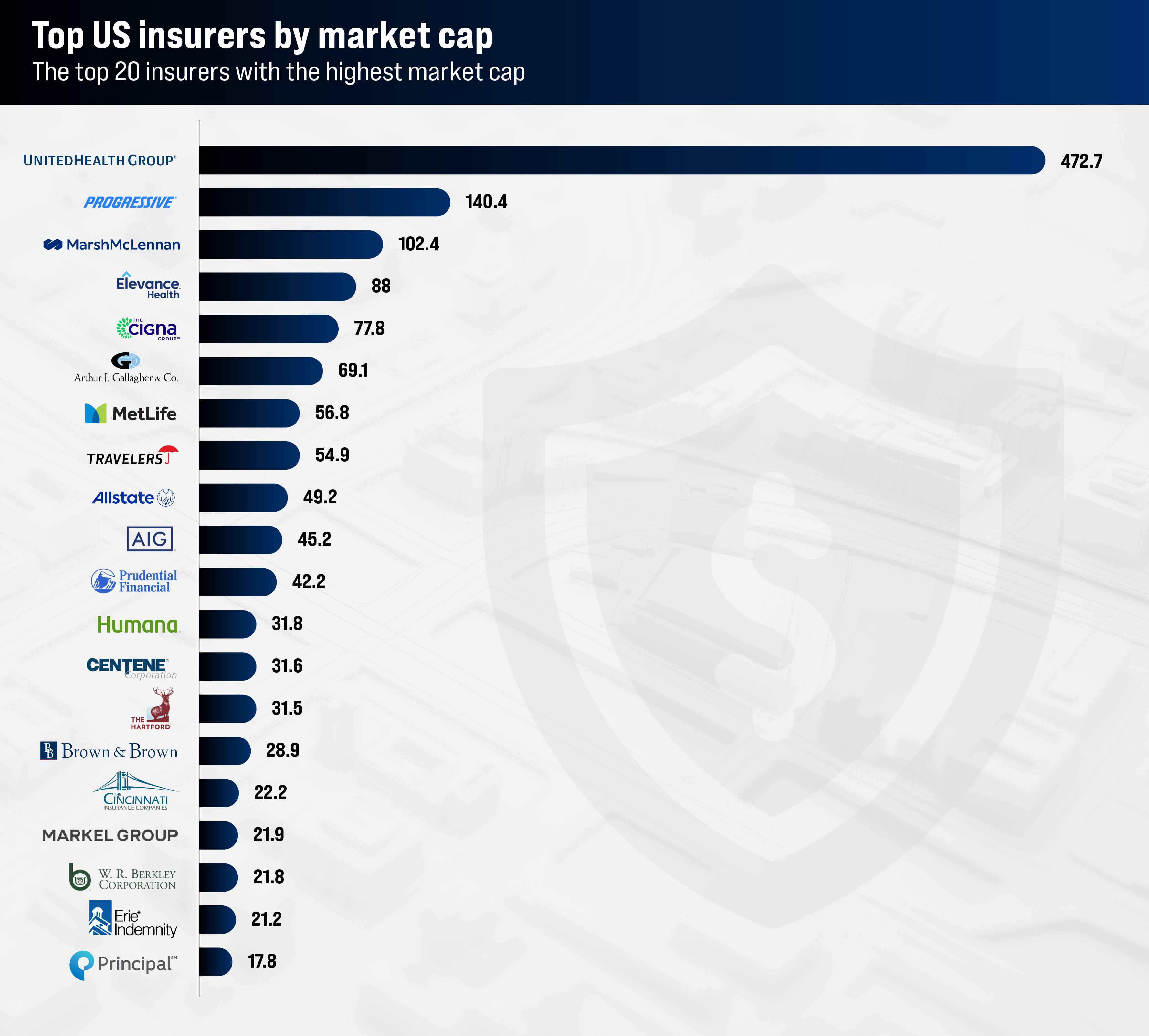

Top U.S. Insurers by market cap

Leading performers like Progressive, MetLife, and Travelers provide brokers with profitable opportunities, driven by robust growth. Meanwhile, health insurers such as UnitedHealth and Elevance may face rising costs but remain dominant in the Medicare and Medicaid markets. For brokers looking to diversify or target niche segments, Markel and W.R. Berkley stand out, specializing in specialty insurance and reinsurance. Each company's strategic positioning presents unique partnership opportunities for brokers, tailored to meet the evolving needs of their clients.

Health insurance sector:

UnitedHealth Group, Elevance Health, Cigna, Humana, and Centene dominate the U.S. health insurance space, with a strong presence in Medicare, Medicaid, and group health plans. Despite challenges, such as rising healthcare costs and regulatory pressures, these companies are well-positioned to sustain growth, especially as the aging population drives demand for healthcare services. Brokers focused on Medicare Advantage and group health plans have significant opportunities in a market where baby boomers are increasingly aging into Medicare eligibility. These companies also present potential for long-term partnerships in healthcare technology and innovation, as they continue to shape the future of the industry.

Property and casualty insurance:

Top players like Progressive, Travelers, The Hartford, W.R. Berkley, and Cincinnati Financial demonstrate strong profitability and consistent growth in property, casualty, and auto insurance. These insurers have shown resilience through effective underwriting and claims management, particularly in auto insurance, business coverage, and commercial property. Given their proven risk mitigation strategies, these companies offer brokers a reliable foundation for expanding their portfolios and managing complex client needs.

Reinsurance and specialty lines:

Markel and W.R. Berkley are well-established in the reinsurance and specialty insurance markets, which include niche commercial lines and specialized coverage such as cyber risk and natural disaster insurance. These companies cater to distinct market needs, making them an ideal fit for brokers looking to provide tailored solutions for clients in high-risk sectors.

Life insurance and retirement planning:

MetLife, Prudential, and Principal Financial lead the life insurance and retirement planning sectors, offering established expertise in individual life policies, retirement solutions, and corporate employee benefits. Companies like Principal Financial and Prudential also present growth opportunities as they expand into investment management and financial advisory services, meeting evolving client demands in a dynamic financial landscape.

Insurance brokers and risk management:

Marsh & McLennan, Arthur J. Gallagher, and Brown & Brown provide significant opportunities in corporate risk management, brokerage, and consulting. These firms excel in managing complex risk portfolios for both large corporations and small businesses, allowing brokers to tap into a broad spectrum of services tailored to a diverse range of clients.

Long-term growth potential:

Insurers with diversified portfolios, such as MetLife, AIG, and Prudential, offer brokers a broad array of products across life insurance, financial services, and commercial insurance. These companies present lower volatility, driven by their focus on core financial products, and are poised for long-term stability and growth.

Global expansion:

With a substantial global presence, companies like Cigna, AIG, and MetLife are strategically positioned to benefit from the expansion of healthcare and insurance services worldwide. Brokers seeking to cater to international clients should focus on partnerships with these firms, which provide global coverage for expatriates, health insurance, and corporate clients in emerging markets. As global healthcare access expands, these insurers offer robust opportunities for brokers targeting global health insurance and employee benefits products.

Technological advancements:

Insurers such as UnitedHealth and Progressive lead the way in integrating cutting-edge technology into their business models, including AI-driven claims processing, predictive underwriting models, and customer service automation. These innovations enhance efficiency and competitiveness, allowing brokers to offer more streamlined, cost-effective solutions to clients.

This data underscores the diverse nature of the U.S. insurance market, with a wide array of opportunities across sectors like health insurance, property and casualty, life insurance, and specialty lines. Brokers can tap into growth areas such as Medicare Advantage, cybersecurity insurance, and employee benefits, while leveraging the stability of established insurers in life insurance and global health markets. Additionally, the increasing use of technology in claims processing, underwriting, and customer engagement presents brokers with significant opportunities to offer innovative solutions to clients.

Brokers should seek to align themselves with insurers that have a strong market presence, robust growth potential, and diversified product offerings, all while being mindful of emerging risks such as healthcare cost inflation, regulatory changes, and cybersecurity threats. With the right strategic partnerships, brokers can navigate the evolving insurance landscape and provide clients with tailored, future-ready solutions.