The insurance industry faces mounting pressure to revisit longstanding commission structures as the Supreme Court prepares to hear a case that could redefine how finance-linked sales are disclosed across the UK’s consumer markets.

The legal challenge - rooted in the motor finance sector - will be heard this week in London’s highest court. But the implications are already rippling well beyond car loans. Senior figures in the insurance sector are increasingly concerned that the court’s eventual ruling could upend the business model behind premium finance - an integral part of how millions of insurance policies are sold and funded each year.

The Financial Conduct Authority (FCA) is already circling. In October last year, it launched a targeted review into premium finance arrangements for motor and home insurance, explicitly citing concerns over the cost and value these credit agreements provide to consumers. “We are particularly focused on protecting financially vulnerable customers and ensuring they receive fair value,” an FCA spokesperson said at the time.

The review - seen by many as a pre-emptive regulatory intervention - has taken on greater urgency in light of the Court of Appeal’s ruling against lenders Close Brothers and FirstRand. That judgment found that commission payments to car dealers were unlawful unless properly disclosed to borrowers. Crucially, the court interpreted that disclosure should be meaningful and specific, not hidden in small print or vague language.

With the FCA now acting as an intervener in the Supreme Court appeal, the financial services industry is bracing for a judgment that could reverberate through every corner of commission-based lending.

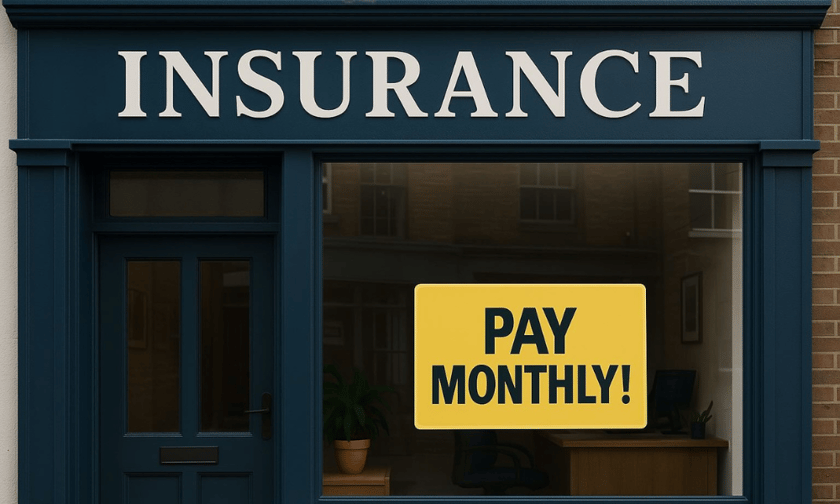

Premium finance, which enables policyholders to spread the cost of insurance via monthly instalments, is widely used by brokers to offer flexibility to consumers. These arrangements, however, are rarely offered for free. In many cases, brokers receive commissions from the finance provider based on the loan value or the interest rate charged - a structure not unlike that used in the motor finance deals now under legal scrutiny.

Benjamin Toms, an analyst at RBC Capital Markets, put the concern plainly in comments to the Financial Times: “Premium finance shares a scary number of similarities. A judgment which encapsulates commissions in all finance arrangements where there’s non-disclosure … will take you beyond motor finance.”

For insurers and intermediaries, the danger is twofold. First, that historic arrangements - going back over a decade - could become the subject of mass complaints or litigation if commissions were not clearly disclosed. Second, that future sales may need to comply with far more stringent standards of transparency, placing pressure on both margins and broker relationships.

Former NatWest chairman Sir Howard Davies has been among those critical of the FCA’s handling of the broader commission issue. Speaking before a Lords committee last year, Davies noted: “I’m disappointed there has not been enough regulatory clarity on the rulebook that has meant the court has been able to step in with its own interpretation.” He added that inconsistent rulings from the Financial Ombudsman Service had only added to investor unease.

While the insurance sector is not yet subject to the same volume of claims as motor finance, that may only be a matter of time. The FCA has already indicated it will decide within six weeks of the Supreme Court ruling whether an industry-wide redress scheme is needed.

“The Supreme Court’s decision will have major ramifications for the financial services market and could kickstart one of the largest and costliest redress schemes since PPI,” said Brian Nimmo, head of redress at financial consultancy Broadstone.

Nimmo also said that the decision, which is not expected until the summer, is set to be a “landmark ruling” that will have broad legal and financial consequences.

“The FCA has already stated that if customers are found to have lost out due to widespread failings by firms, it would consult on an industry-wide redress scheme to avoid an individual case-by-case approach and establish a consistent framework for compensating consumers,” Nimmo added.

Read more: Brokers on MGAs

Should the court uphold the earlier ruling in full, insurers with in-house finance arms - or those who rely heavily on third-party credit providers - may face renewed scrutiny. Insurers may need to revise documentation, re-examine historic disclosures, and consider provisioning for potential liabilities. The exposure could be particularly acute among brokers offering premium finance to lower-income or vulnerable customers.

At stake is not only the cost of redress, but also the regulatory foundation on which decades of commission-based distribution have been built. As one compliance head at a major insurer remarked privately, “It’s not just about car loans anymore. It’s about whether anyone selling financial products through a broker has been entirely upfront about who’s getting paid - and how much.”

For now, the industry watches and waits, but the message from the regulators and the courts is clear: transparency is no longer optional. It is the price of trust - and potentially the cost of survival.