The current era of “polycrisis,” marked by overlapping and interconnected challenges - from climate change and rapid technological advancements like AI to geopolitical tensions - demands a proactive approach to risk management, according to Christoph Nabholz (pictured), chief research and sustainability officer at the Swiss Re Institute.

Insurers that understand and can address these interwoven risks can position their organizations for success. “If we understand what these risks are going to contribute, we will understand the risk landscape, and we know what products will be needed in the future,” Nabholz told an audience of insurtech and insurance leaders at ITC London, which opened in the UK capital on Monday (January 27).

He stressed that addressing interwoven risks is key for businesses and governments to unlock transformative opportunities, from accelerating the net-zero transition and harnessing digitalization to stabilizing supply chains and driving sustainable economic growth.

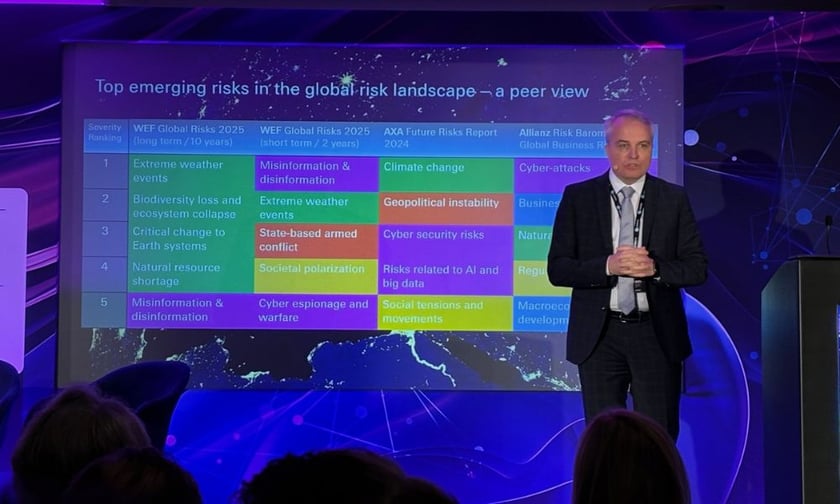

Nabholz named three main risk clusters impacting organizations worldwide:

Climate risks are long-term (10 years and more) and primarily nature-related: climate change, biodiversity loss, and natural disasters. In contrast, digital risks (such as disinformation and cyber threats) and socio-economic risks (such as geopolitical tensions) are more short-term (two years).

Climate risks are a particular focus as insured losses from natural disasters exceeded $100 billion in 2024 for the fifth consecutive year, Nabholz said.

"If you focus on the data, the climate risk column is undeniable, it's everywhere,” said Nabholz. “Biodiversity loss, climate change, and extreme weather are clear priorities for the next decade."

Beyond property damage, cascading effects such as infrastructure failures, water contamination, and supply chain disruptions highlight the interconnectedness of risks. The Swiss Re Institute leader also cited the ongoing wildfires in Los Angeles as an example, with the disaster causing damage to infrastructure like roads and water systems.

Climate risks also include infrastructure vulnerabilities and the long-term impacts of renewable energy. For instance, the lifecycle challenges of solar panels, wind turbines, and battery farms pose recycling and liability risks. Nabholz said that while green infrastructure investment is essential, it comes with a raft of new exposures, including environmental liabilities and workplace risks.

Moreover, health-related outcomes, such as respiratory and cardiovascular diseases linked to climate change, further complicate the risk landscape. These developments underline the need for innovative insurance products that address both property and casualty risks, as well as health-related exposures.

At the same time, digital risks are accelerating, fueled by the rapid adoption of artificial intelligence (AI). Exposures such as failure risks, ethical concerns, and “silent cyber” risks - where algorithms autonomously adapt - could bring unintended outcomes for organizations.

"AI is growing at a 38% compound annual rate, and soon it will be bigger than the internet. But its failures, especially in healthcare or underwriting, are creating new risks,” said Nabholz.

Nabholz cited the July 2024 CrowdStrike incident, where a single software update disrupted eight million systems, causing $10 billion in losses within 24 hours. This event, he said, underscores the growing dependency on big tech and the systemic risks posed by failures in critical digital infrastructure.

Other risks in the digital cluster include cyber-enabled fraud and social media-driven instability. For example, the collapse of Silicon Valley Bank in 2023 demonstrated how rapid digital withdrawals can destabilize financial institutions, creating cascading effects throughout the economy.

Finally, social inflation and the growth of so-called “nuclear” verdicts leading to large claims is driving significant change in the casualty and liability markets, especially in the US, Nabholz said. Combined with technology-enabled litigation recruitment, this is creating an environment where insurers are constantly on the back foot.

At the same time, economic losses from supply chain disruptions are expected to grow, with a $150-billion coverage gap.

Despite these challenges, Nabholz remained optimistic, pointing to emerging opportunities for the insurance industry.

New technologies, such as biometric monitoring and FemTech solutions, present avenues to address gaps in healthcare, particularly for underserved populations. The executive highlighted the potential for AI to revolutionize customer engagement, predictive maintenance, and risk assessment.

By embracing innovation and collaboration, the industry can turn risks into opportunities, Nabholz said, ensuring a sustainable future for insurers and their customers.

What interconnected risks pose the biggest concern for your organization? Please share a comment below.