At the 2024 CFC Summit, group CEO Louise O’Shea and distribution director Pat Brice addressed the elephant in the room in a room populated by hundreds of insurance brokers – are there foreseeable circumstances under which CFC might open a direct channel and retail insurance directly to consumers?

For Brice, the answer was unequivocal – “just no”.

As distribution director, he said, he recognises the role of the broker in offering advice to customers, a role which is especially critical in a fast-evolving risk landscape such as the one facing clients today. That advisory role is not what CFC does for a living, it exists to build insurance products, services and propositions, and to deliver them. Clients’ needs are evolving all the time, and it’s CFC’s role to get ahead of that change and build products to mitigate its impact.

“Your job is to be their partner,” he said. “Your job is to advise them. Your job is to find the right markets for them… We’ve got no business working directly with clients, in terms of selling business to them. We will work directly with you and partner with them on cyber risk, through the app and things like that. But I categorically can’t see [going direct].”

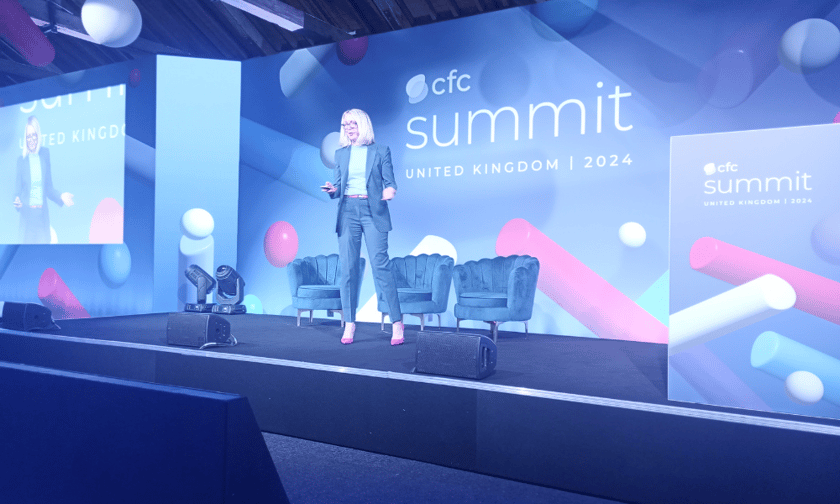

Hailing from a direct retail insurance background as the former CEO of Confused.com, O’Shea (pictured) affirmed the firm’s distribution strategy, joking that Brice doesn’t need to be concerned about his job description changing. She noted that when she ran Confused.com, the company had 20 million customers and played to a very different market – personal lines.

She pointed to the essential role that CFC’s broker partners play in translating exceptionally complex insurance topics to customers. “That’s not our business, that’s your business,” she said. “We’re in the business of identifying how we can best support you, be that through additional material, or whatever will help you do your role.

“Fundamentally, we’re about creating new products. We’re about looking to the future, at the new risks that are coming, and working out how we can support our joint, combined customers in protecting themselves against that. So no, categorically, there’s absolutely no plan for us to go direct to consumer.”

Looking to the future, O’Shea, who is less than a year in the top seat at CFC, outlined what’s next for the business, which has got, “a lot going on”. Looking at how the business has grown over the years, she said she has been impressed by the speed with which it moves to respond to the evolutions of the market and she believes all the right ingredients are in place for CFC to fulfil its vision of becoming the insurance business of the future. “The challenge, of course, is going to be preserving the very best of what CFC has [here…] while simultaneously growing into a much bigger company.

“We plan to scale to be one of the biggest players in our market, and our current focus is on sustained, rapid growth. So how are we going to do this? Well, we’re going to go deeper into our existing markets. We’re entering new markets every day, and we’re launching new products. Now is the time for CFC to move… closer to our global customers, enabling us to reach further and serve our customers better.”

O’Shea highlighted that when it comes to growth, quality is what really counts. “In a world where so many of our interactions are being automated away, there is going to be an increasing disparity between commoditised offerings and the players who protect what cannot be replicated,” she said.

“I’ve seen this firsthand in the aggregation market of personal lines. So, I know the pitfalls for the customer, for the broker, for the insurer… I believe in order to be irreplaceable, one must always be different, distinctive and special.”

O’Shea earmarked CFC’s people & culture, technology and data as key areas for investment in the coming years. On geographic expansion plans, she outlined the plan to capture what’s made the business thrive in the UK, and replicate that formula for growth. She identified its acquisition of Solution Underwriting in Australia as an example.

With Kate Della Mora appointed CEO of CFC Canada earlier this year, joining Shannon Groeber, CEO of CFC in the US, the firm now has people operating in Toronto, New York and San Francisco. “And watch this space,” O’Shea advised. “We’ll be having people in continental Europe very soon. While we’re working on all this international growth, we’re still very much focused on our home market, the UK. We’re building out our regional distribution capability in order to improve our visibility and accessibility to you.”