Best Insurance Companies for Construction in the UK |

5-Star Construction

Jump to winners | Jump to methodology

Laying the foundations

Insurance Business UK celebrates the 5-Star Construction winners of 2024, the result of canvassing hundreds of brokers across the country to provide their industry knowledge and feedback on insurers.

In addition, brokerages were also surveyed by IBUK to detail what brokers value in the best construction insurers. The firms that received the highest rankings in work quality, specialist expertise and client service were awarded 5-Star status.

Showcasing the high standard and demands of the sector, 80% of IBUK’s 2024 winners also triumphed in the previous report, 12 months ago. This pattern was struck upon by brokers, who shared their valuable insight with IBUK by stating that they like to see greater competition in the marketplace. Other themes also resulted from the brokers’ feedback.

The first was a desire to see more appetite for bespoke policies, as one broker respondent says, “As insurance processes become more automated, I am seeing less flexibility. I would like underwriters to be a bit more flexible. As an example, there’s no meaningful difference between falling off something 15 meters tall and falling off something 16 meters tall; arguably, falling from a greater height is better from the claim point of view. But a lot of insurers will say, ‘The computer says no’ if you tell them you’re working at 16-meter heights.”

The second theme was protecting client information with the proliferation of data breaches. On this issue, a broker says, “I would like to see more protection of sensitive customer data from cyber threats, and ensuring compliance with stringent data protection regulations are paramount challenges in safeguarding the industry’s reputation and maintaining customer trust.”

More demand for best construction insurance companies

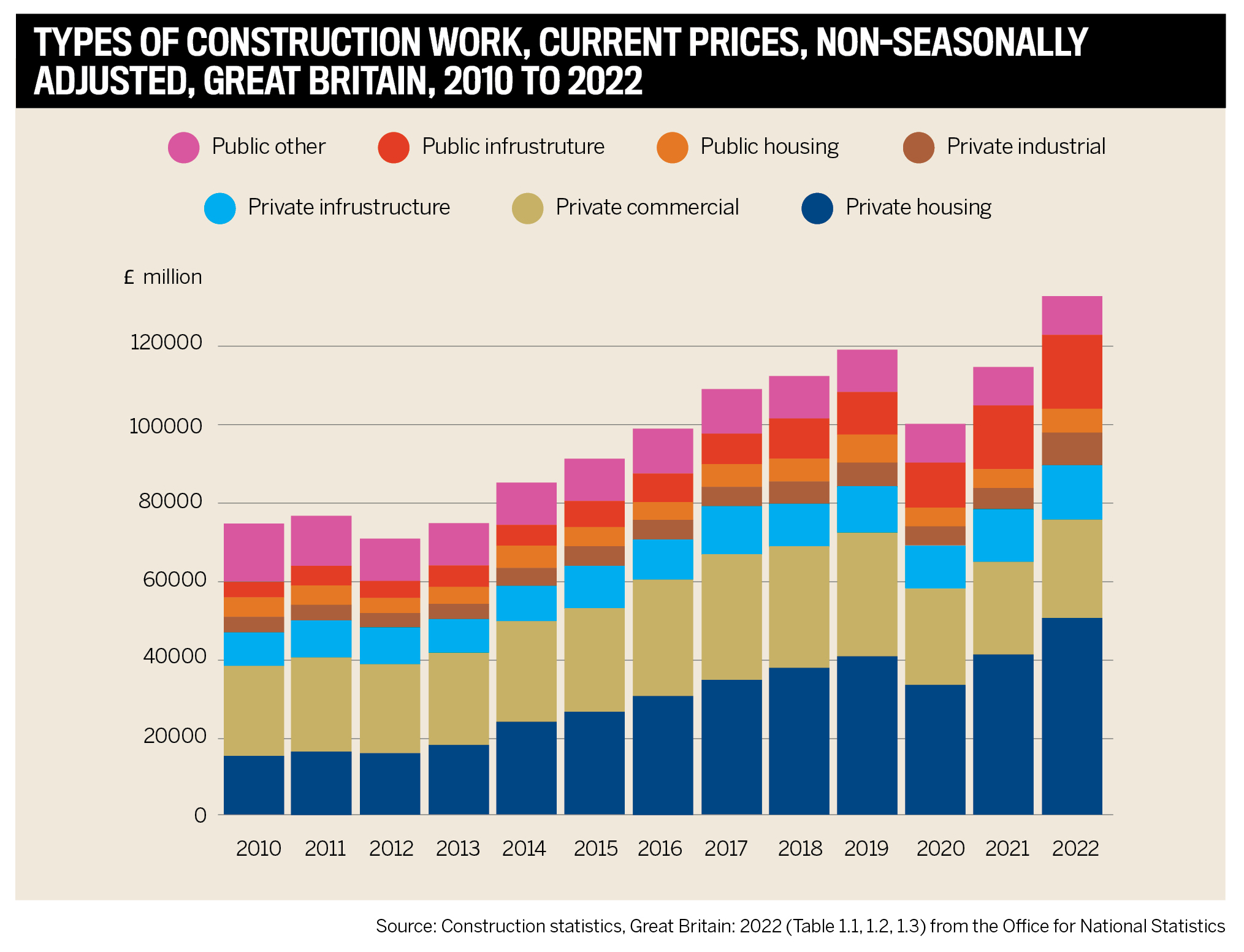

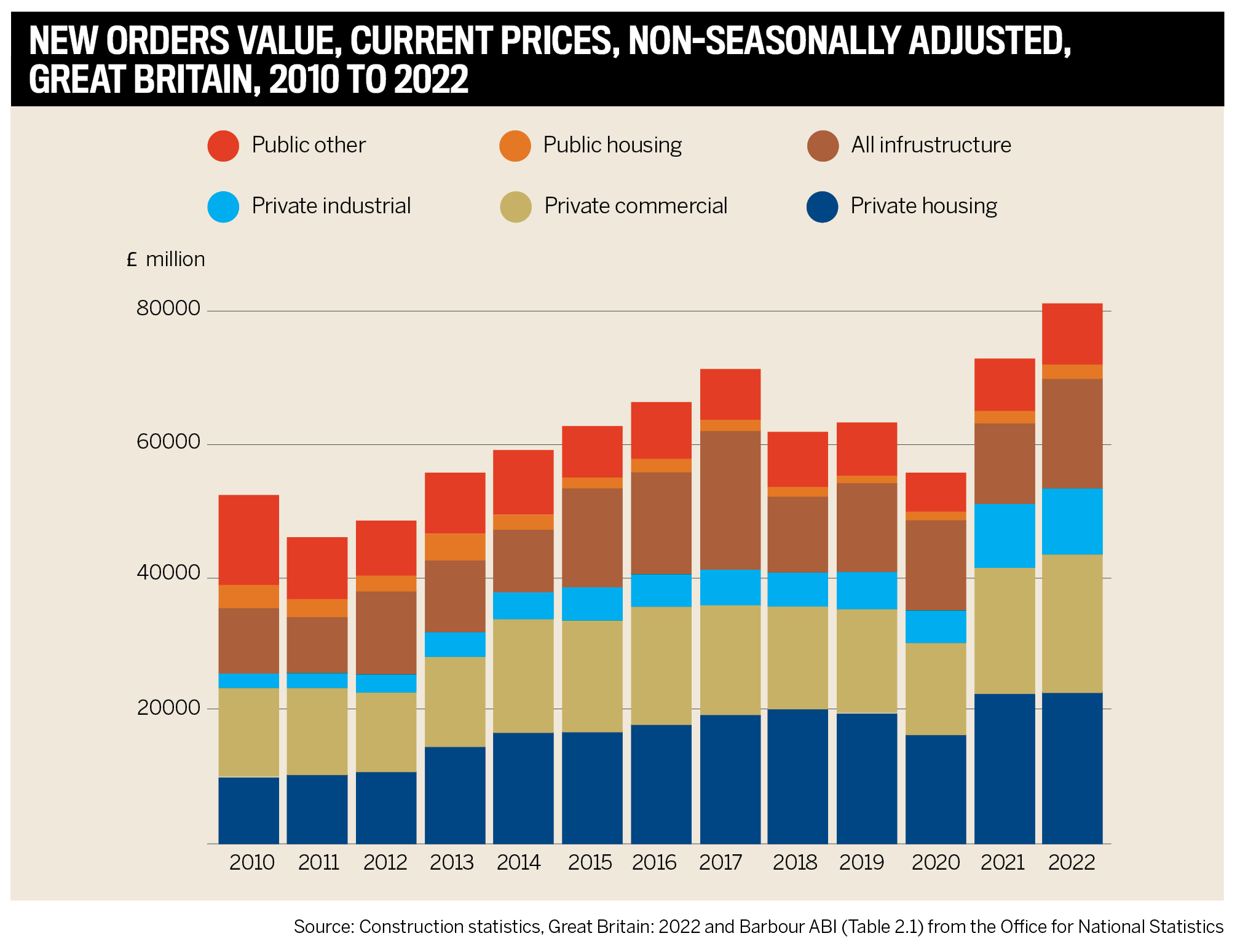

Data shows the need for construction insurance is on the rise in the UK.

The value of construction new work in 2022 increased 15.8% to a record high of £132,989 million; this was driven by growth in both private sector work of £14,093 million and in the public sector of £4,068 million.

In addition, annual new construction orders in 2022 increased 11.4% to a record high value of £80,837 million. The main contributors were private infrastructure, private commercial and other public non-housing, which increased 85.1%, 10.2%, and 17.5%, respectively. This was slightly offset by the private industry, which decreased by 0.6%.

The need for greater insurance is also highlighted in project management consultants Currie & Brown’s UK construction market outlook for 2024. Their analysis states:

-

“We anticipate an increase in construction activity, which could strain the currently limited labour and contracting resources.”

-

“Despite the near-term slowdown, the data underscores an enduring need for housing and infrastructure development. Those companies that position themselves strategically can be well placed to capitalise on the eventual recovery.”

-

“With contractors expanding out of their core markets or project scales, clients can potentially tap into a wider range of expertise and experience by considering contractors venturing outside their comfort zones. This could open doors to new possibilities and be beneficial for complex projects requiring a broader skill set.”

Purbeck Insurance Services reported that more builders and SME construction firms opted to apply for finance to support growth and development in 2024’s O2, which is more than at any other time in the previous 18 months.

Todd Davison, managing director of Purbeck Insurance Services, says, “As the government pledges to build 1.5 million homes in England over the next five years to ‘get Britain building again,’ our data suggests renewed confidence among businesses in the sector, despite major challenges around skills availability.”

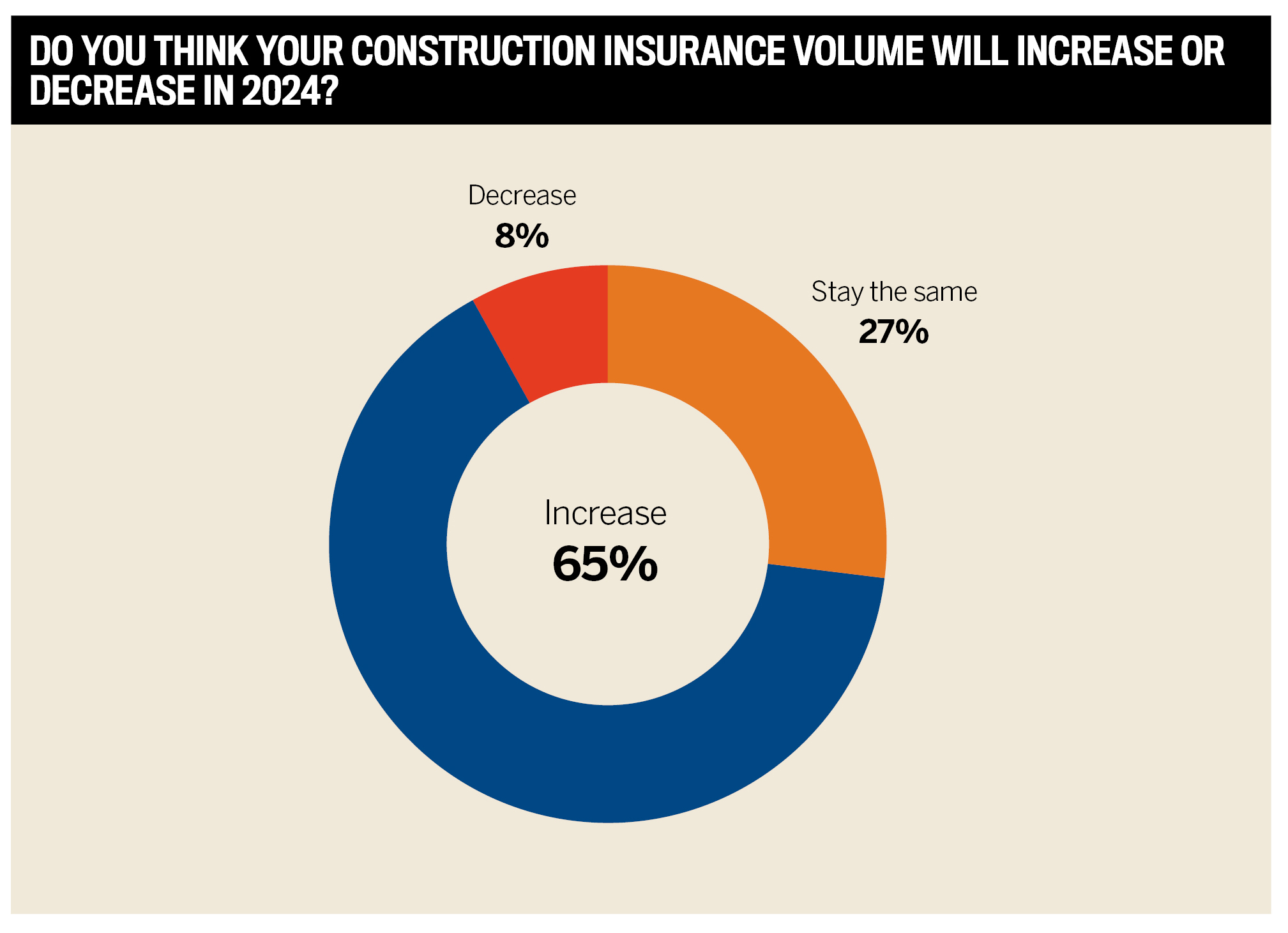

A rise is expected in total premiums, but rates should remain competitive, according to David Widdick, placement broker at Verlingue.

“The construction sector has suffered from a higher-than-average amount of insolvencies, which has given some insurers cause for concern, but we know there is investment and capacity out there for quality construction companies that will drive competition and lower rates,” he says. “The casualty market has been less volatile than the property and financial markets in the last five years, and insurers have been securing inflation increases without much opposition, so there should be scope for keen pricing.”

The brokers who took part in IBUK’s survey seem to share these sentiments, as 65% expect the rise in construction to be reflected in a rise in premiums.

What is 5-Star Construction insurance?

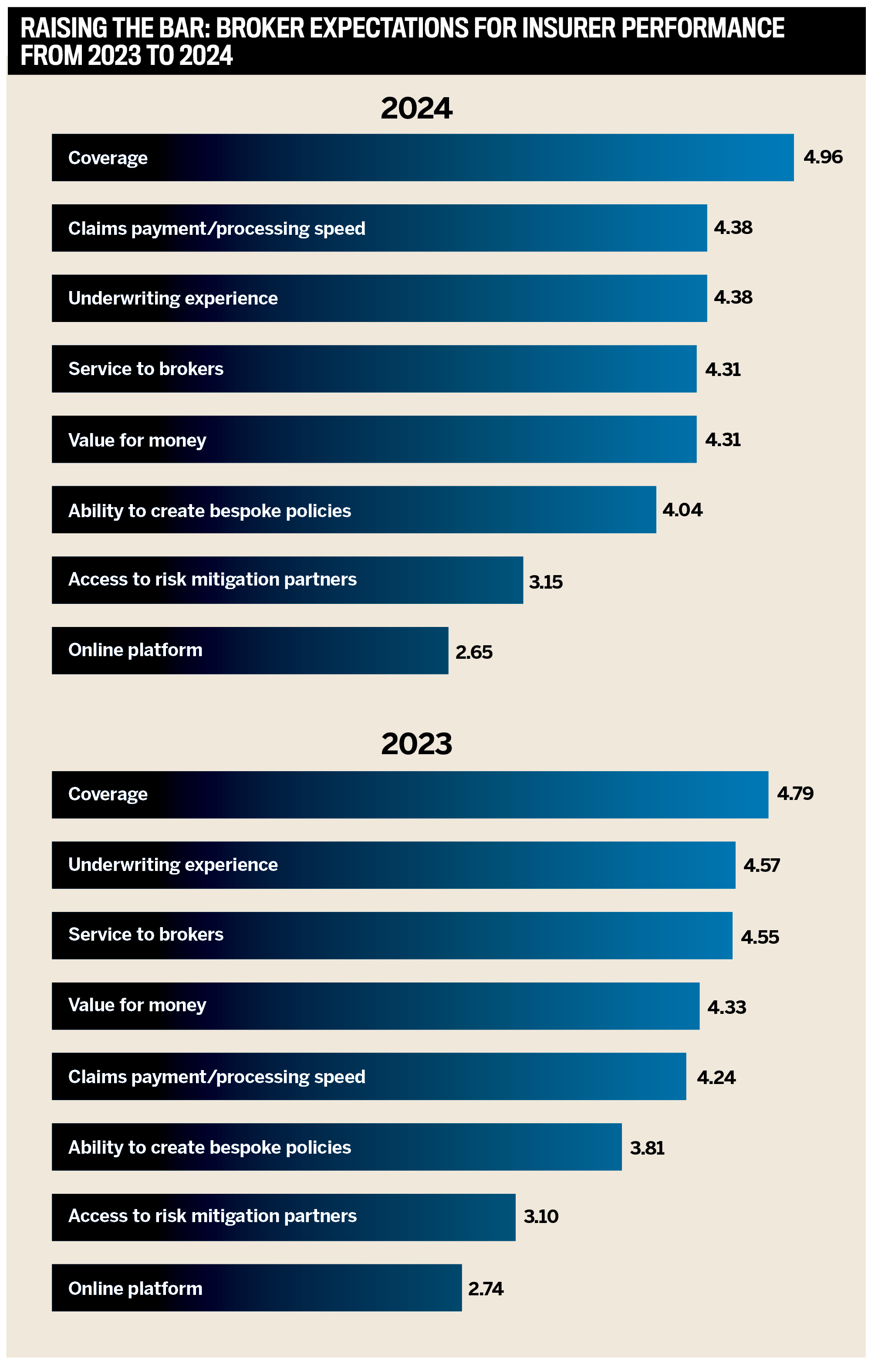

IBUK asked brokers about construction insurers specifically in relation to eight criteria and to rate each between one and five.

Comparing 2024’s data with that from 2023 shows that coverage remains the most important factor for brokers, and its average rating increased by 0.15.

However, claims payment/processing speed has become the joint second most important issue, along with underwriting experience in 2024, whereas 12 months ago it was only the fifth biggest factor. The bottom three features of ability to create bespoke policies, access to risk mitigation partners and online platform were the same in both years.

Overall, in 2024, six of the eight criteria scored over 4.0, but in 2023, this was five, which suggests brokers are expecting and wanting more comprehensive all-round policies/service from insurers.

A trio of industry experts shared their insights into what matters in the themes connected to IBUK’s 5-Star Construction criteria:

-

Tracy Keep, development director and client services manager for construction at Gallagher

-

David Widdick, placement broker at Verlingue

-

James Fairclough, assistant claims director – property, casualty and specialty at Verlingue

Coverage: “The extent of each can be very different; for example, many public liability policies do not provide the part products liability extension, which is crucial for new construction projects. Contract works cover is often only arranged on a DE3 basis, but enhanced cover can be provided for a small additional premium under DE4 wording. It is imperative that all contractors consider arranging professional indemnity insurance, as some still tend to have the belief that coverage is solely for designers. Many different contractors have a contingent professional indemnity exposure, and it is important that this is discussed with contractors who may not realise they in fact have an exposure.” – TK

Underwriting experience: “Underwriting authority needs to be senior enough to make the big decisions quickly. Increasingly, we are concerned with underwriting being too data led. While it no doubt brings advantages, sometimes this appears to be at the expense of common sense.” – DW

Value for money: “Costs can differ significantly from project to project, and with the market now ‘softening,’ we are seeing rates stabilise for clients, which is very welcome as they face significant cost pressures from all areas. In respect of hidden fees, the market operates in a very transparent manner, but the one thing we always remind our clients of is the importance of making sure their insurances comply with the contract requirements, or they can face a charge to amend them later, which they often haven’t budgeted for.” – TK

Claims payment/processing speed: “Top-performing insurers are expected to process and settle claims in a reasonable and fair time as soon as the claim has been quantified and liability accepted under the policy. However, if this is not possible, insurers should consider prompt interim payments, usually within 14 days, to ensure adequate cash flow, which will afford the policyholder the opportunity to mitigate their losses and immediately rectify any issues arising from their negligence. Prompt payments are crucial in the construction and contract work sectors, as unnecessary delays can lead to escalating hire charges for replacement machinery, particularly when dealing with high-value equipment that often has significant lead times.” – JF

Bespoke policies: “Within the parameters of their appetite, this is essential. Where it is disappointing is when an insurer expresses an appetite for a particular trade within construction but is completely immovable around the risk transfer needs of that business. If insurers want to segment by trade, then they should write down all the risks of that trade.” – DW

Online platform and tech: “One of the key factors we are seeing insurers improve upon is their rating for construction projects, which is being facilitated by various factors such as more accurate flood maps and analytics showing how quality risk management can help reduce risk. Significant improvements have also been made in insurers mobile apps, which have improved claims reporting processes and employee training, which is a step in the right direction for the industry. We’re also seeing insurers partner with innovative companies such as Risk Talk to help clients modernise their processes and various vehicle tracking companies to help clients improve their fleet risk.” – TK

Broker recommendations and industry trends

Despite the 5-Star Construction insurers delivering for the market, there are a range of initiatives that the UK brokering community would like to see adopted.

Some of their feedback included:

-

“More access to underwriters and less use of online platforms.”

-

“Improved timeline from insurers for resolving coverage queries/disputes.”

-

“More capacity for MMC, e.g., Timber Framed and more competitive PI Insurance.”

-

“Additional underwriter training for brokers.”

-

“Wider appetite for heavier trade sectors from more insurers.”

-

“More package type offerings for the smaller contractors, along with more of a focus and ease in terms of bonds, guarantees, etc.”

-

“More cover for contractor insolvency, refreshers on DSU review for SME, and cessation of works clauses to be increased/more flexible.”

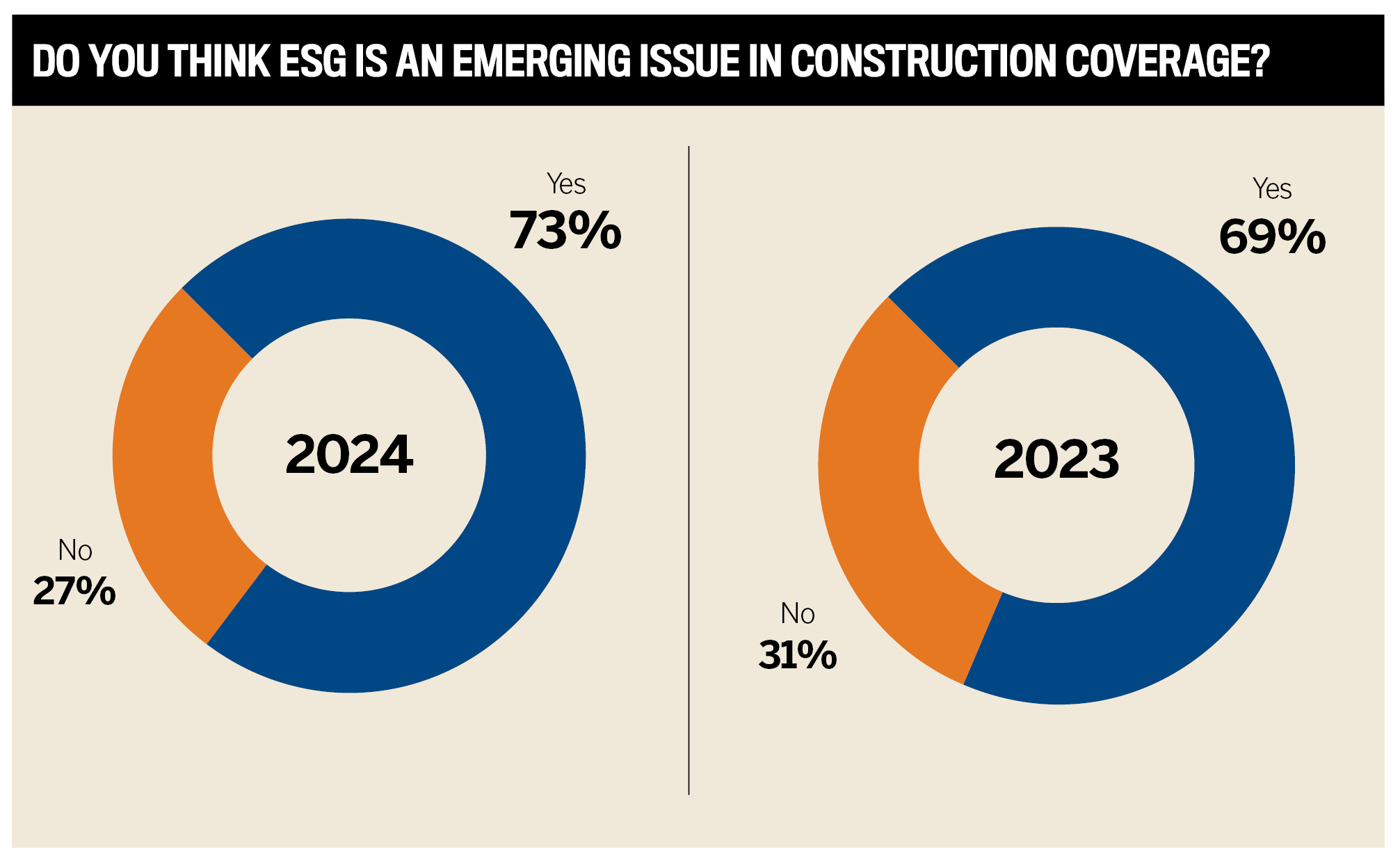

Another factor that insurers need to be aware of is the rise in ESG. IBUK’s data show that between 2023 and 2024, the number of respondent brokers who cited it as an ‘emerging issue’ rose by 4%.

The issue is highlighted in EY’s benchmarking study on ESG reporting in the engineering and construction industry (February 2024) particularly on what types of materials are used and the concept of circular building, which delivers projects that need less maintenance and are easier to repair, thus having a material impact on insurance costs and are easier to repair, thus having a material impact on insurance costs.

Their report states, “Circular building optimises the use of resources and minimises waste throughout a building’s whole life cycle. The design, operation and deconstruction maximise value over time by using durable products and services made of secondary, nontoxic, sustainably sourced, renewable, reusable or recyclable materials. Additional value can arise from an increase in a structure’s space efficiency over time through shared occupancy, flexibility and adaptability. This will also add longevity, resiliency, durability and easy maintenance and reparability.”

A further major ESG impact on construction insurance is coming from climate change, as a marked rise in the number of extreme weather events (floods, fires and droughts) and the resulting damage are pushing premiums higher.

EY’s study concludes, “These impacts include faster degradation of construction materials, like corrosion of metals and shorter life spans of wooden buildings, leading to structural damage. Water damage and leaks can lead to mould growth, and a sudden shift in energy use can increase HVAC usage and cause higher operational costs. To mitigate these risks, the industry must apply climate-resilient solutions, including building codes that support sustainable construction and address risks connected with climate change. Construction companies need to provide appropriate health and safety conditions for workers at the site, including preparedness for extreme weather events and natural disasters. Using climate-resilient design and materials and solutions suitable to mitigate the impacts of climate change is a must for a more sustainable future.”

Therefore, by taking ESG issues into consideration more, the industry will ensure a longer life span for projects, easier repairs and safer conditions for workers, which will ultimately have a positive impact on the insurance cost and burden.

Widdick adds, “With planning law driving more sustainable construction, I would say it is now second nature for many contractors to investigate the environmental credentials of their suppliers. At Verlingue, we are lucky to cover businesses innovating in the sustainable construction supply chain, so we get to see the changes in action. Tender documents require evidence as a standard of a broker’s ESG policy as well as that of its insurer partners.”

He also highlights some ESG-related products that impress him.

“QBE’s Premiums4Good is an excellent way for a business to ensure its money goes to the right place,” says Widdick. “QBE’s Minds in Business, promoting a risk management approach to employee mental health, is forward-looking and admirable in an industry where over 700 people take their own lives every year.”

Best Insurance Companies for Construction in the UK | 5-Star Construction

- Allianz

- Aviva

- AXA

- IIGL

- QBE

Insights

Methodology

To select the best construction insurers for 2024, Insurance Business UK sourced feedback from insurance brokers. IBUK’s research team began by conducting a survey of a wide range of brokerages to determine what brokers valued in a construction insurer. The team also spoke to hundreds of brokers across the country, asking them to rate the construction insurers they had worked with over the past 12 months.

The in-depth information gathered enabled the research team to assign weighted values to each of the criteria being rated by brokers. At the end of the research period, the insurers that received the highest rankings in terms of work quality, specialist expertise and client service were named 5-Star award winners in construction insurance.

Keep up with the latest news and events

Join our mailing list, it’s free!