Fastest-Growing Insurance Brokerage

Companies and MGAs in Canada

Jump to winners | Jump to methodology

Masters of scale

Insurance Business Canada’s fastest-growing brokerages and MGAs are riding the crest of a wave after recording an impressive couple of years by delivering in a changing landscape. The need to grow and adapt is the result of insurers seeking agile, tech-enabled firms to manage complex risks while retaining the fundamentals of speed and efficiency.

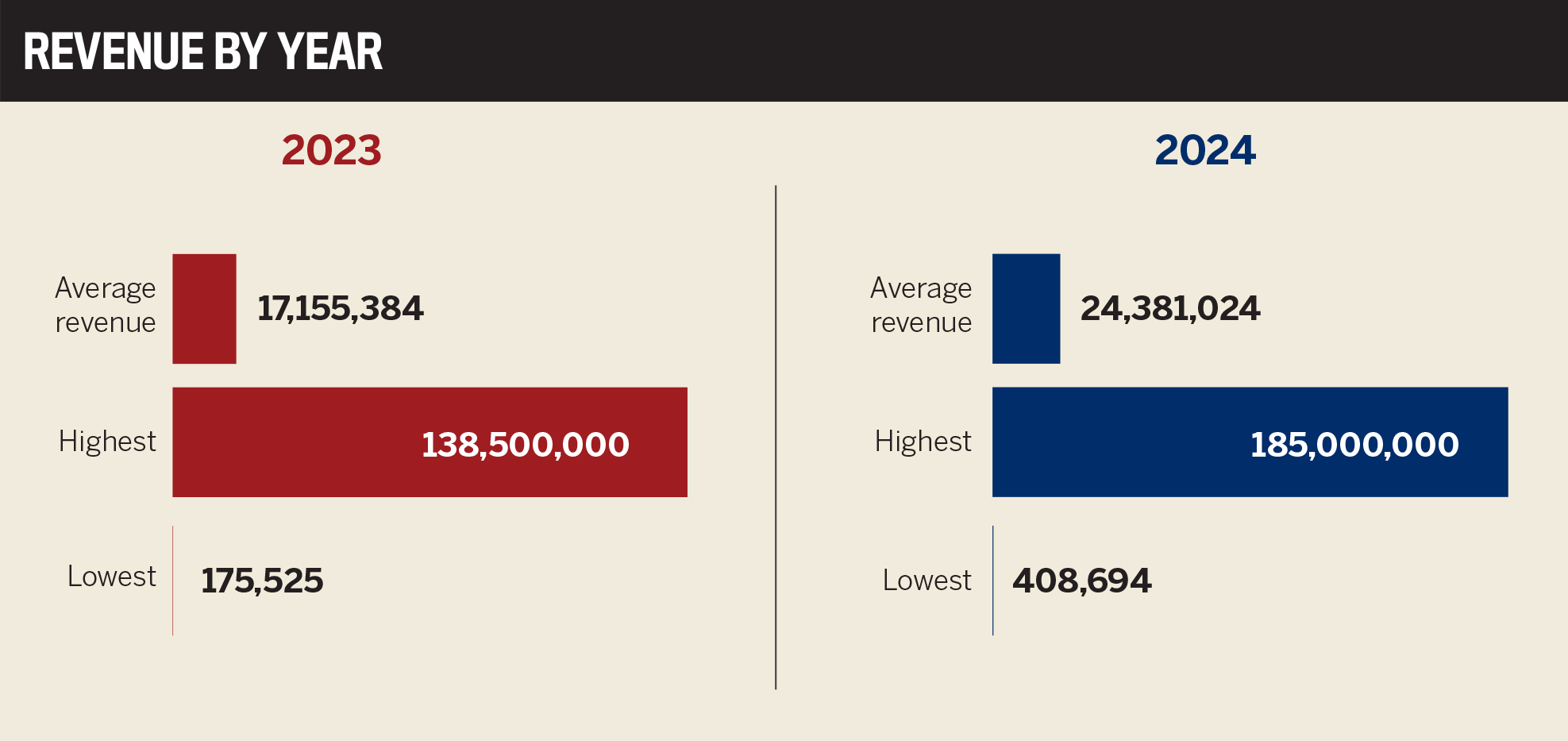

Between 2023 and 2024, this year’s Fast Brokerages and MGAs pushed average revenue up by 42 percent, jumping from $17.2 million to $24.4 million. Some saw even bigger gains as one MGA surged from $138.5 million to $185 million, while a four-person brokerage more than doubled its revenue.

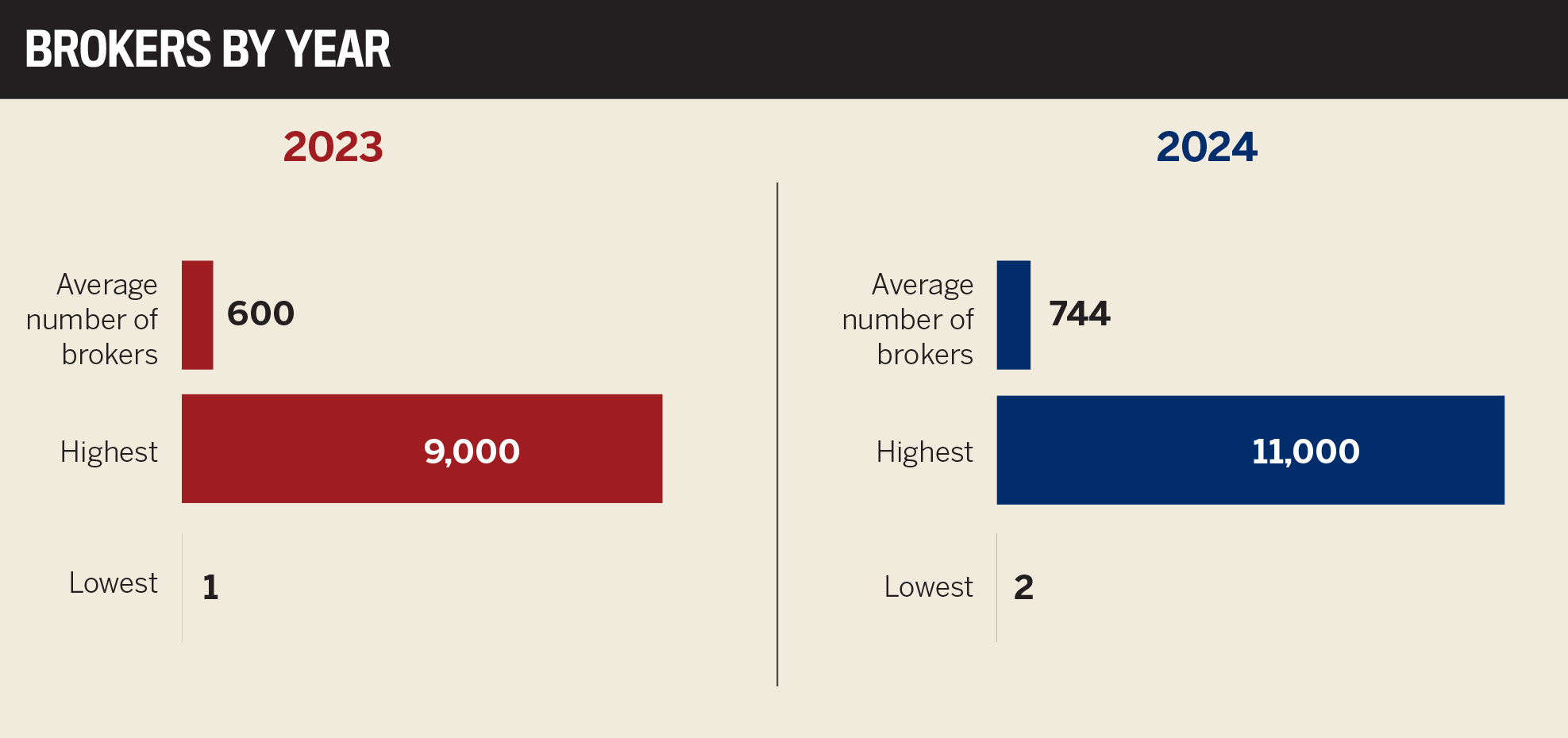

IBC’s data shows that expansion, acquisitions, and sharper operations have all played a role, raising the bar with revenue growth averaging 50 percent. The average number of brokers per company also grew by 24 percent, boosted by hiring and scaling strategies.

Keeping pace with the market is a challenge, and the leading firms are proving that growth involves a combination of strategy, agility, and the ability to move when the moment is right.

KPMG Canada’s partner and managing director of corporate finance, Andrew Mathias, explains that achieving growth is particularly impressive due to the mature nature of the Canadian market.

He highlights the ways to grow as:

-

M&A

-

stealing market share from another group

-

cross-selling

“Unless you have a capital sponsor like private equity or carrier backing, M&A is extremely expensive and, in a lot of cases, not accretive because you are overpaying,” says Mathias. “Stealing someone’s market share is tough because they also want to defend, and there are many people competing for the same piece of the pie.”

Cross-selling is the easiest of the options but requires a wider portfolio of lines of business.

For the brokerages that have achieved growth, Mathias underlines how important the fundamentals are.

He says, “They have to really execute on customer service excellence and ensure they’re overservicing clients with significant expertise in niche lines of business.”

Mitch Insurance CEO Adam Mitchell shared his insights on the changing market in terms of marketing and how people connect, highlighting that the fundamentals of growth still ring true.

“You need to retain the clients you had last year to build on top of them; otherwise, you get the leaky bucket effect,” he says. “You also need to find new leads and have the ability to close those leads. What’s changing is how you get those leads, as marketing has changed a lot over the last five years.”

Success now means scaling, innovating, and pushing forward to maintain momentum.

Mitchell asserts there’s no silver bullet for growth and emphasizes the need to measure all efforts.

He says, “If you’re not tracking where your leads are coming from, which ones close, and your acquisition costs, you don’t know which channel to optimize. Even networking time needs to be measured. If you’re generating leads through industry events, you need to consider the time investment and how scalable that is.”

Over the past 18 months, IBC’s top performers have hit significant milestones, including:

-

completing high-impact acquisitions and expanding into new provinces

-

attaining commercial, property, and casualty (CPC) accreditation with multiple carriers

-

gaining a competitive advantage as the first to offer Lloyd’s of London property insurance for cannabis

-

underwriting 100 percent of advertised products in-house under a delegated authority agreement

-

adopting cutting-edge technology, digital initiatives, automation, and cloud migration

-

developing new industry-leading products

-

expanding workforce, advisor networks, and partnerships

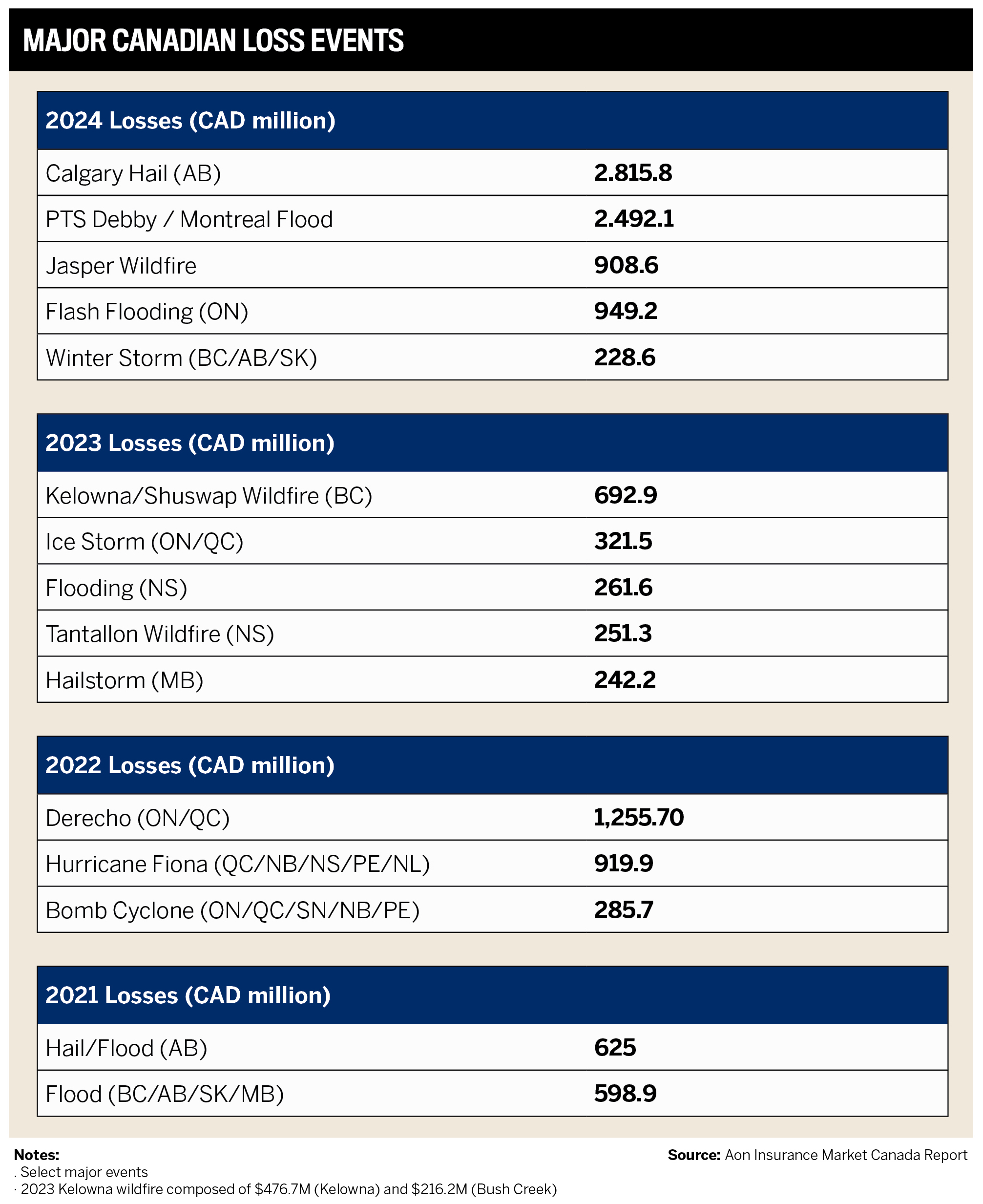

This growth comes despite an increasingly unpredictable P&C market, with catastrophic losses that surpassed $7.6 billion by September 2024, the highest on record, according to Aon’s Fall 2024 Insurance Market Update Canada report.

Heading into 2025, the fastest-growing brokerages and MGAs are continuing to adapt as the industry shifts. Canadian insurers already faced nearly $9 billion in catastrophe-related losses in 2024, and new pressures are emerging, states a report by Morningstar DBRS.

That financial storm is predicted to ensure property insurance rates keep rising, and reinsurance costs could also increase.

“There’s a lot of discussion around auto reform and whether that will change the priority of payments,” Mitchell says. “There was also talk about car dealerships being able to get licensed and sell insurance directly. Right now, an insurance brokerage is not allowed to work with and share commission with a dealership, yet regulators are discussing enabling direct sales inside dealerships. There’s a disconnect in the regulations. I think those two issues could be interesting disturbances.”

However, commercial lines are expected to see price moderation, creating opportunities for the growing number of companies to capitalize on shifting market conditions.

One specific line that’s emerging is cyber insurance, but the challenge is consumer demand, and brokers are still in an education phase.

Mitchell says, “Other lines will grow at the pace of inflation and immigration. Otherwise, growth comes from competition, whether it be other distributors, direct writers, or brokers. If you’re trying to take business away from others, you have to figure out how you can compete and how you’re going to win.”

For fast-growing MGAs and brokerages, staying ahead means building on underwriting expertise, strong carrier relationships, and technology-driven solutions.

Industry insider Mitchell notes that brokerages not using a lead management system to track progress are missing opportunities.

“That means your total closing rate is low, your acquisition cost is quite high, and you won’t sustain growth compared to the competitors,” he says. “Consumers also want self-service options, which is pretty difficult for brokers to implement meaningfully.”

He adds, “The biggest shift in the past 18 months is the depth of AI, and it has been a game-changer.

“There are hundreds of tools and integrations that brokers can use. In the next 18 months, you’re going to see many brokerages strip out certain costs, and if they reinvest that back into marketing and other areas, the game really will change.”

Mitchell emphasizes that the ability to provide fast, tailored placements for complex risks will become even more crucial as the market continues to evolve.

Despite these pressures, the top-performing brokerages and MGAs continue to lead by investing in advanced technology, specialized underwriting talent, and best-in-class customer service.

IBC’s 2025 winners have been able to carry out strategic expansion and implement innovation to fast-track success in a highly competitive Canadian casualty market.

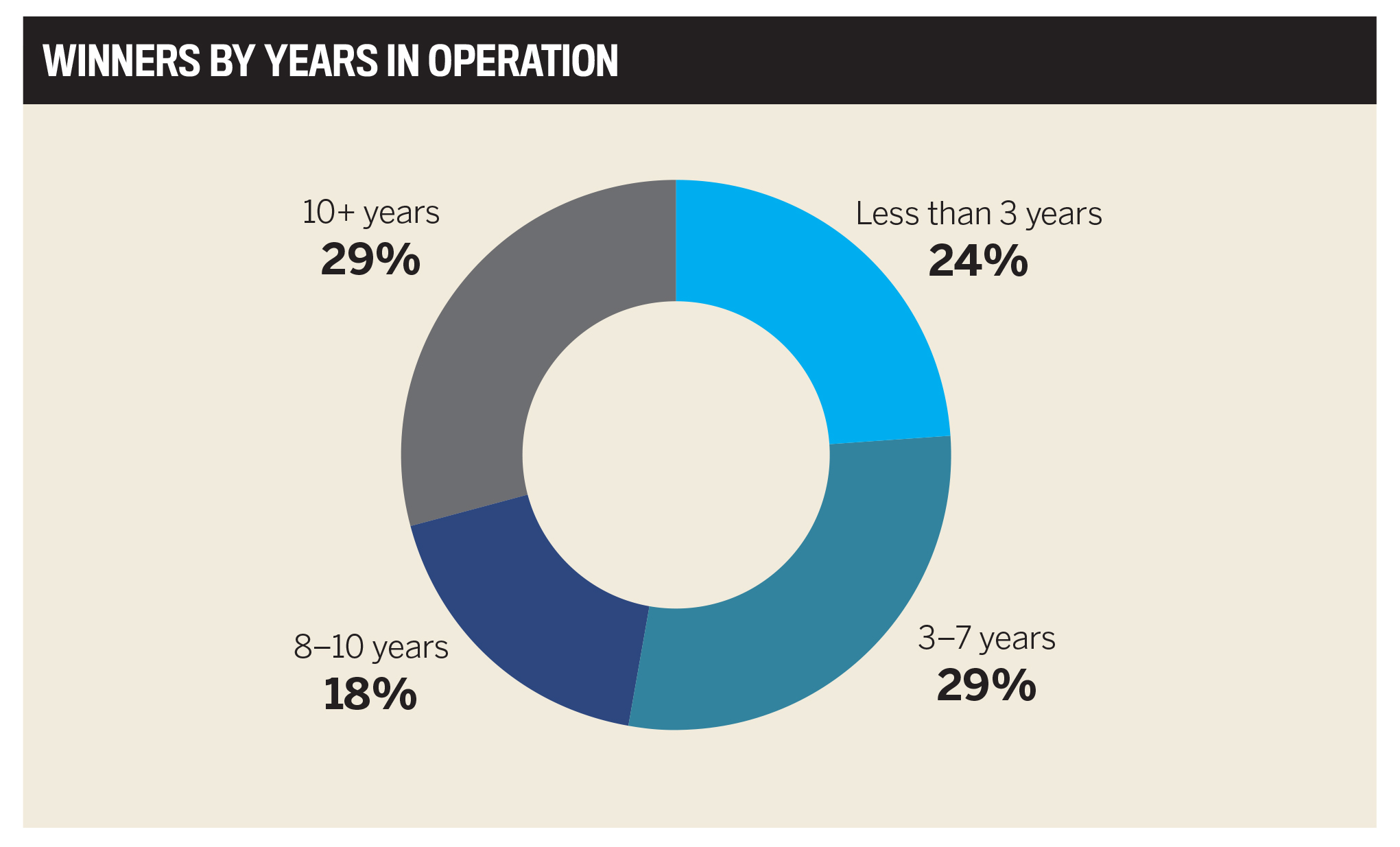

A subset of winners, Fast Starters, have been in business for three years or less. These firms have only known challenging conditions, including a hard market turning soft, tech advancements, rising inflation, and an increase in natural catastrophes.

Mathias says, “Brokerages that were able to navigate the headwinds and succeed in the first three years must have been built with rock-solid infrastructure and support with razor-focused leaders to steer the ship.”

Fastest-growing insurance brokerages and MGAs leading the next wave

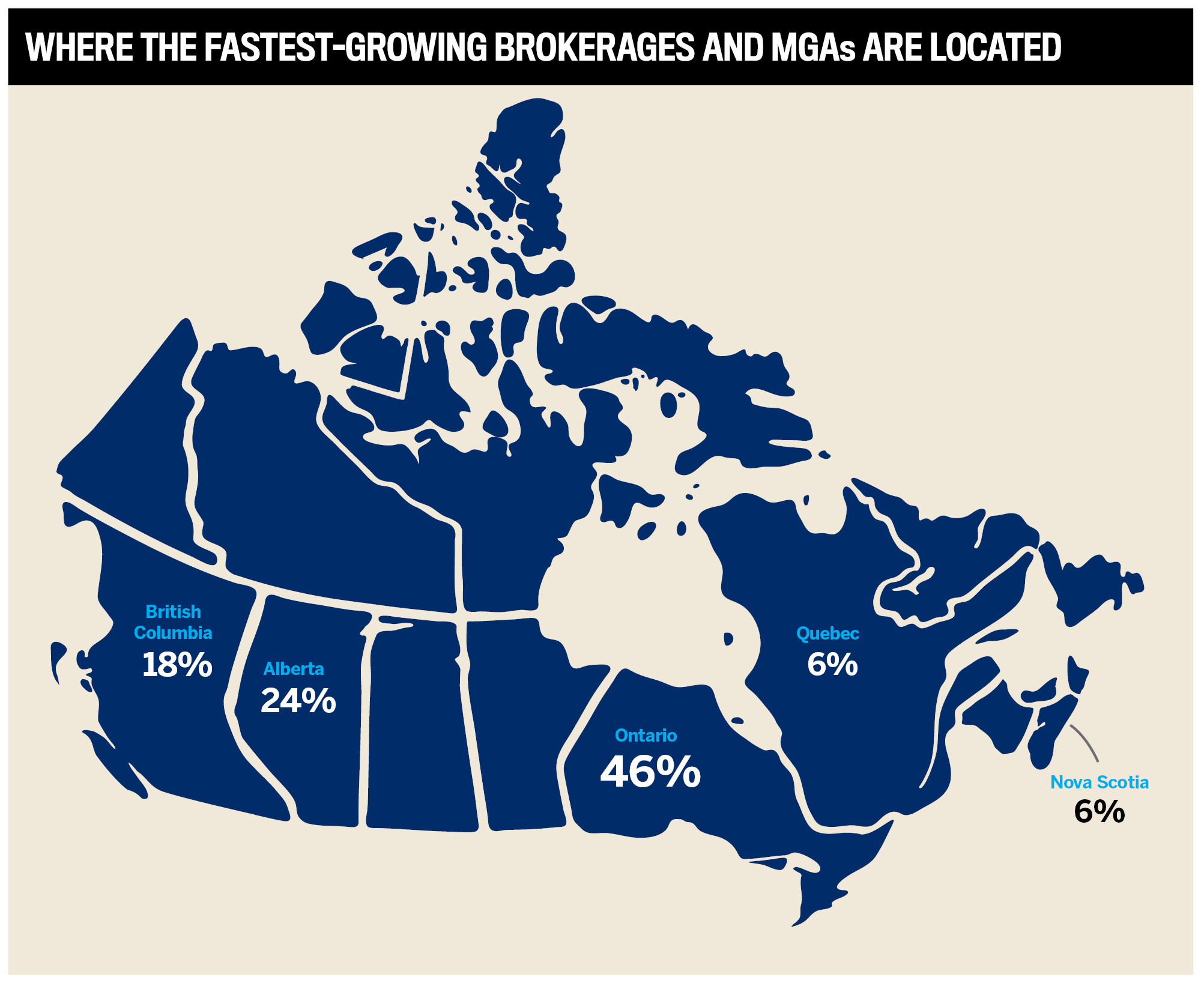

IBC recognizes 17 companies nationwide that achieved at least 20 percent revenue growth in 2023 and 2024, including five MGAs and 12 brokerages.

Four of these firms earned Fast Starter distinction for achieving standout revenue growth within three years of launching.

Together, they posted a striking 74.75 percent average revenue increase, setting a new benchmark for ambitious newcomers.

Starting a brokerage today is different from when Mitchell started. Early on, insurance websites were rare, and brokers approached online interactions with caution. But today’s brokers need a strong digital presence to stay relevant.

At the same time, industry consolidation has shifted insurer focus toward billion-dollar brokerages.

“For small players, a single misstep could blow a marketing budget, or losing a key carrier relationship can set them back significantly,” says Mitchell. “The pace of new start-ups isn’t keeping up with the pace of exits, which means fewer and fewer small players are entering the market.”

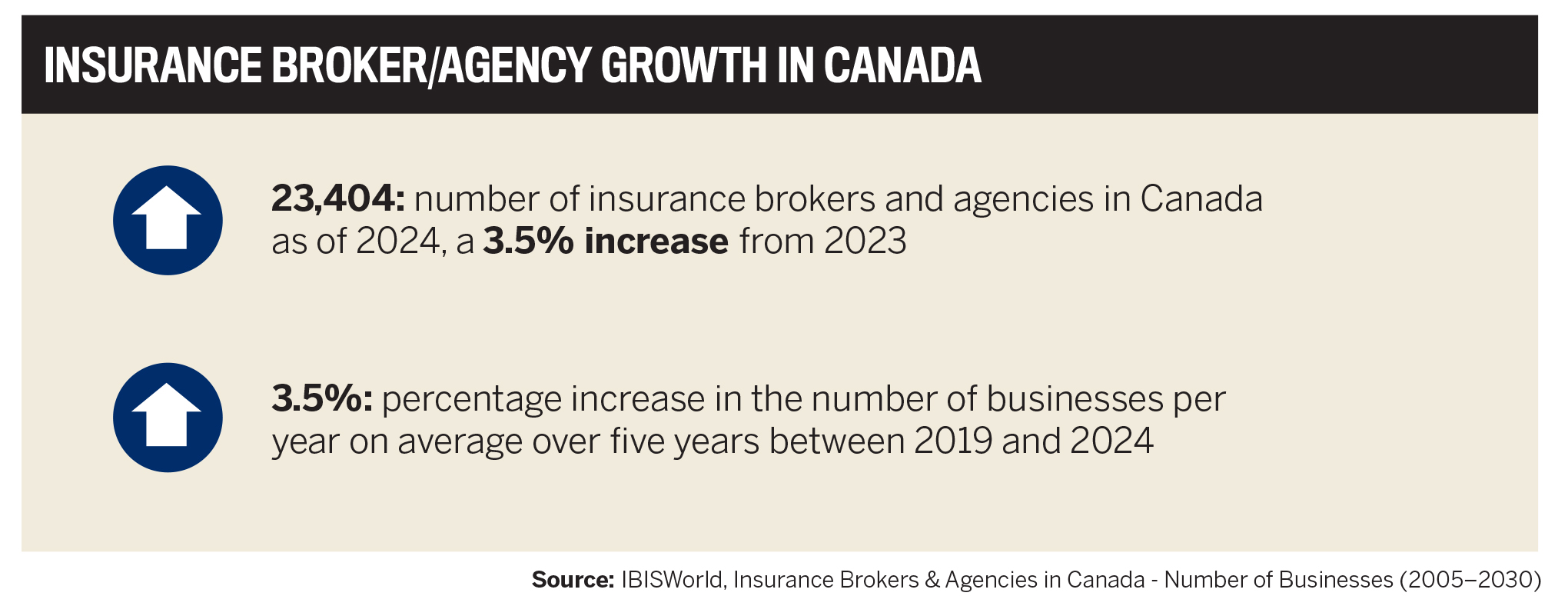

Their collective growth reflects broader trends in Canada’s insurance market, where competition and specialization intensify (see the chart below).

Among IBC’s 2025 winners is NovaRisk, a Toronto-based managing general underwriter that exemplifies the speed, creativity, and expertise demanded in Canada’s fastest-growing market.

Long-standing relationships in the broker community and a reputation for handling complex commercial risks have shaped the firm’s rise from startup to top-tier MGA.

“Our guiding philosophy is that with extensive professional underwriting combined with the right investment in technology, an MGA can deliver unparalleled top- and bottom-line value to like-minded partners,” managing director Maz Moini says.

Maz MoiniNovaRisk

Backed by cutting-edge technology, NovaRisk’s integrated underwriting and financial platform provides a clear edge over legacy carrier systems, enabling fast service to brokers.

Armed with ample domestic A-rated delegated underwriting capacity, the company has established a strong position in the Canadian insurance market since launching in 2022. Its fast growth defines the bold expansion and industry leadership shown across this year’s winning Fast Brokerages and MGAs.

Founded by a team of former insurance company executives with a proven track record in growing insurance portfolios, NovaRisk set out to offer extensive domestic underwriting capacity, in-house underwriting, and claims expertise, giving brokers a compelling, made-in-Canada placement option.

From the start, its goal was to build a legacy-free platform that supported a future-focused business model. It operates 100 percent paperless on a proprietary, fully integrated end-to-end system, from submission intake to financial statements.

NovaRisk’s ability to provide fast and fair underwriting solutions has helped it capture market share in an increasingly competitive sector.

2023 and 2024 growth highlights include:

-

generating a strong submission pipeline and achieving quote ratios in the high 40s, which is widely acknowledged as above average

-

doubling revenue, broker appointments, and underwriting capacity year over year

-

securing national licensing

-

launching an internally developed MGA system

“We have been fortunate to have received strong broker support from our early days in operation,” Moini says. “We believe that’s due, in large part, to the reputation and relationships that our underwriting team enjoys with brokers from coast to coast.”

A culture that supports and retains talent

NovaRisk’s broker strategy has played a key role in its momentum, including:

-

targeting complex accounts: partnering with brokers’ offices to handle complex clients and projects that require expert underwriting and a strong understanding of higher-hazard exposures. The goal is to create solutions that effectively deploy the carrier’s capacity at an appropriate rate.

-

prioritizing select broker relationships: working with a chosen group nationwide to maintain high service levels and ensure fast, informed decision-making.

The leadership team has intentionally fostered a collaborative, ethical, and positive work environment by treating everyone respectfully.

That approach has helped attract top talent, ranging from industry veterans to recent graduates. It proudly boasts an ethnically diverse, 12-person team with a 40-60 male-to-female split, all essential for a small, fast-growing company.

“We’re recruiting at the moment, and one of the things that we specifically look for, apart from technical skills, even for a junior position, is cultural fit,” Moini says. “We’ve attracted really good talent when we can guarantee they’re coming into a positive, supportive culture where everybody helps each other.”

The company also offers a hybrid-plus work policy, allowing employees to decide how they split their time between working from home and at the physical office, in the true spirit of flexibility and sensitivity to their needs.

Meeting industry challenges head-on

MGAs like NovaRisk exist to bridge market inefficiencies, filling the gaps when carriers and brokers struggle to secure timely client solutions.

“The industry faces no shortage of challenges, from underwriting talent gaps to elevated catastrophic losses,” Moini says. “MGAs need to shine when times are tough. NovaRisk has supported brokers and carriers through the turbulence of COVID-19, the fallout from defunct MGAs, and now the structural economic shifts arising from US tariffs.”

Commercial property, commercial casualty, and builders’ risk are key elements accelerating the Fast Starter’s growth. Powered by a strong domestic panel of (re)insurers, its expert underwriters deliver capacity to accounts and projects across the country.

NovaRisk differentiates itself by providing fast responses, fair terms, and a focus on appetite-fit submissions. That formula works as brokers send in over $100 million in P&C submissions annually, proving its market impact and value.

For new firms looking to succeed in today’s market, Mitchell says that sales solve a lot of problems.

“Get good at sales, which means getting good at finding leads,” he says. “Once you find leads, track them, analyze them, and improve your approach. Track your acquisition costs and expenses closely.

“And I’ll take the words from an insurance broker friend of mine, who said there are only 8–10 major insurance companies in Canada and millions of Canadians that buy the product. Don’t get those ratios confused. You need to have those valuable relationships with the insurance company. So, respect that trust. And work hard to build it.”

Moini shares a similar perspective on the importance of strong industry relationships, noting, “Our expansion is guided by the needs of our brokers and carrier partners. We see ample opportunity to better service our brokers in existing product lines by geography and with increasing underwriting bandwidth. We also expect to introduce new product lines and verticals in 2025 and 2026.”

For example, NovaRisk launched an umbrella product offering for its brokers in early 2025. Plans are also in place to scale its new entertainment vertical nationally, following a successful soft launch in 2024 that received excellent broker feedback due to the team’s deep underwriting expertise in this segment.

Later in 2025, the company anticipates expanding its underwriting capacity in Quebec to better service its broker partners in that province by offering higher property and casualty limits across all segments.

Fastest-Growing Insurance Brokerage

Companies and MGAs in Canada

Fastest-Growing Brokerages and MGAs 2025

- Agile Underwriting Solutions

- APOLLO Insurance

- Axis Insurance Managers

- Beyond Insurance

- BMS Canada Risk Services

- Carte Risk Management

- InsureLine Brokers (Empire)

- InsureLine Brokers (Premier)

- Mango Insurance

- MaxxCann Insurance Services

- Oakway Insurance

- OVC Assurance

- RH Insurance

- Scoop Insurance Brokers

- SIGNAL Underwriting

- Verdant Insurance

Insights

Methodology

Insurance Business Canada invited submissions for its Fast Brokerages and MGAs awards in November 2024 as the publication sought to recognize brokerages across the country that excel during challenging circumstances. The research team asked brokerages and MGAs to list their revenue totals for the 2023 and 2024 calendar years, in addition to other growth milestones they wanted to highlight. The team then evaluated the nominations received to determine which firms experienced standout growth.

The 2025 Fast Brokerages and MGAs awards are given to companies that achieved more than 20 percent growth in revenue volume. IBC also highlights four firms as Fast Starters, which have been in business for three years or less and are making their mark on the insurance landscape. These companies confirmed their resilience and cemented their strong positions in the Canadian insurance industry.

Keep up with the latest news and events

Join our mailing list, it’s free!