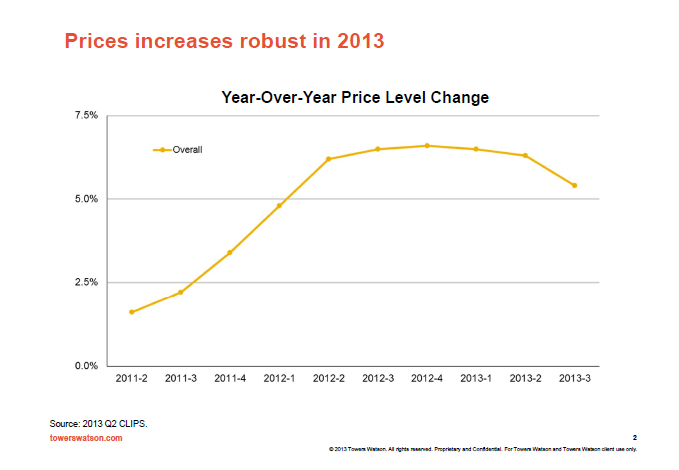

Prices for commercial insurance lines continue to increase, though at a slightly slower rate, Towers Watson’s most recent Commercial Lines Insurance Pricing Survey (CLIPS) found. According to the agency’s report, the prices for commercial policies written during 2013’s third quarter increased by 5%—a somewhat smaller increase than the 6% and 7% boosts seen in previous quarters.

Nevertheless, prices for all commercial lines are up—particularly in employment practices liability, which saw price increases jump into double digits. Workers compensation and commercial auto followed closely behind in terms of the highest increases.

Towers Watson also found that mid-market accounts saw the largest increase in prices, while prices for large and small accounts increased at lower rates. Specialty lines prices also saw less of an increase than standard lines.

For producers, these overall higher prices mean a potential boost in profits, said Tom Hettinger, Towers Watson’s Property & Casualty sales and practice leader for the Americas. However, with that perk comes a greater responsibility, Hettinger told Insurance Business.

“Price increases mean better commission fees for brokers, but higher expectations from customers for services received with fees paid,” Hettinger said. “If all ships rise, customers will not have much negotiating power, but they may still look due to the price increases and ask, what do they get with the dollars they pay to differentiate the different companies?”

That’s a trend Ty Sagalow, president of the consultancy firm Innovation Insurance Group, has forecast as well. According to Sagalow, price increases mean producers will need to seek out policies that provide more value-added services that reflect the changing needs of the client.

“This is yet another good example of the need for innovation in the insurance industry,” Sagalow said. “With these changes, we need modification of insurance policies. We have to keep abreast of the times and make sure our policies reflect those.”