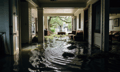

Besides waging his ongoing war against illegal immigration, President Donald Trump has also recently criticized the Federal Emergency Management Agency (FEMA) for its handling of disaster relief efforts, particularly in response to Hurricane Helene in North Carolina.

During a tour of the state, he suggested that FEMA has been ineffective and proposed either overhauling or eliminating the agency, favoring direct federal funding to state governments for disaster management.

These remarks have since sparked discussions about the future of federal disaster response, with some experts expressing concern over the potential impacts of dismantling FEMA.

While some critics have argued that it could undermine coordinated national efforts in managing large-scale emergencies, some insurance brokers are cautiously optimistic, viewing the potential changes as a chance for private insurers and companies to take on a greater role in disaster recovery.

"Changes to FEMA (and the NFIP) represent opportunity for the insurance industry," said Dana Sutton, AVP, personal risk, flood practice at NFP. "It could lead people to move from the NFIP into the private market, which is an overall net good for the industry. More risk moving in the direction of the private market means lower rates and expanded coverages."

Sutton, who spoke with Insurance Business a few weeks ago to discuss the current state of flood insurance and the growing role of the private market, said that she believes a revamp is worth discussing, particularly given concerns about the agency’s slow response time.

"I would welcome a discussion about a FEMA revamp," she said. "Based on feedback from clients, the immediate response to storm events this past hurricane season was somewhat slow, so there seems to be room for improvement."

However, Sutton also argued that improvements should extend beyond just disaster response.

"I’d also love to see more resources put into flood proofing and mitigation efforts. FEMA did a study that showed for every $1 spent on mitigation efforts, it saved $6 in flood losses," she explained. "As flooding events increase in frequency and severity, flood proofing and mitigation are great courses of action, and FEMA should continue to lean into these efforts."

One of the broader concerns surrounding potential FEMA changes is whether the private insurance market could fully replace its disaster response functions. Sutton made a clear distinction between the role of FEMA and the role of insurers.

"The private market’s role in responding to a disaster is inherently different than FEMA’s role or should be," she said. "The private insurance market’s role is to support the rebuild after the loss – to make people whole again. FEMA’s response should be more focused on basic human needs following a catastrophe, such as safety, food, shelter, and access to medical care."

She also emphasized that while private insurers play a key role in financial recovery, emergency response efforts need to be structured differently. "Once a disaster area is stabilized, people can work with their carrier to rebuild.”

Another important aspect of a potential FEMA overhaul is how it might influence public perception of disaster relief.

"There is also a perception that after a flooding event, FEMA will bail you out," Sutton said. "If this perceived safety net is gone, perhaps it would encourage people to be more proactive in their own efforts to mitigate their individual risk."

She noted that while FEMA provides assistance, it is often limited and cannot replace full insurance coverage. A reduced FEMA role could shift more responsibility onto individuals and businesses to ensure they have adequate insurance policies and risk mitigation strategies in place.

From a broker’s perspective, Sutton stressed that regardless of FEMA’s future, policyholders must take proactive steps to protect themselves.

"This is the most important part of this entire discussion," she said. "Regardless of what does or doesn’t happen with FEMA, we can all individually manage our individual exposure better."

Sutton also advocated for greater awareness and preparedness when it comes to flood risk.

"People should be proactive in their own risk mitigation. Speak to a trusted and knowledgeable insurance advisor about your actual flood risk. Everyone should have a flood policy, regardless of their flood zone," she said. "If your insurance agent tells you that you don’t need a flood policy, find a new agent."

She also highlighted the importance of personal preparedness, especially as extreme weather events become more common.

"Heed all the cautionary warnings that continue to come out of the large-scale unexpected flood losses: It can happen to you, and you can be better prepared for it," she said. "Have supplies ready and an exit plan should you need to evacuate the area. If you are sheltering in place, be prepared to shelter for at least a week."

In addition to individual preparedness, Sutton urged people to consider their communities as well.

"Reach out to friends, family, and neighbors who may be more vulnerable or unable to help themselves and be ready to assist them when and where you can," she said.

What are your thoughts on this story? Please feel free to share your comments below.