Insurance in the US is regulated at the state level. This means each state has its own statutes and rules on which types of insurance coverage are mandatory.

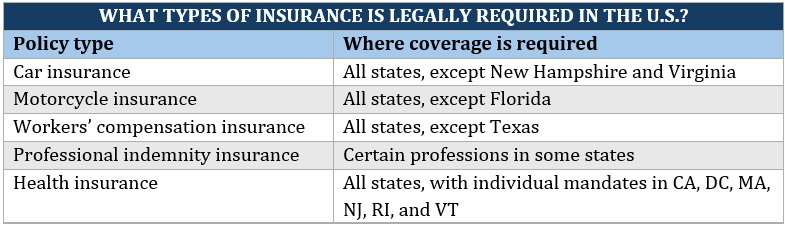

There are three main types of insurance coverage required in almost all states:

Health insurance is no longer required at the federal level, although some states still impose tax penalties for those who don’t have coverage.

Some states also make it compulsory for certain occupations to carry professional indemnity insurance.

If you want to learn more about what insurance is required by law in the US, Insurance Business gives you a state-by-state breakdown per policy type in this guide. Read on and find out.

Car insurance, also called auto insurance, is designed to protect you financially if you get into an accident or your vehicle is stolen. This policy provides three kinds of protection:

Car insurance is required by law in all states, except in New Hampshire and Virginia.

In New Hampshire, drivers are only required to show proof of their financial capability to cover for injuries and damages for accidents that they cause.

In Virginia, motorists can opt out of coverage if they can provide evidence of financial responsibility. For drivers who choose to be uninsured, they will need to pay a $500 uninsured motor vehicle (UMV) fee at the state’s Department of Motor Vehicle.

The remaining states impose varying requirements, including the policy type and minimum liability limits. Here’s a summary of the common types of car insurance:

Here’s a state-by-state breakdown of the mandatory coverages and minimum liability limits:

|

MINIMUM MANDATORY CAR INSURANCE LIMITS BY STATE |

|

|

State |

Minimum mandatory requirements |

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $50,000 per person BI: $100,000 per accident PD: $25,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $15,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $15,000 per person BI: $30,000 per accident PD: $5,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $15,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $10,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident UM/UIM PD: $5,000 |

|

|

BI: $25,000 per person BI: $50,000 per accident BI: $10,000 per accident PIP: $15,000 per person PIP: $30,000 per accident |

|

|

PD: $10,000 per accident PIP: $10,000 per person |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $20,000 per person BI: $40,000 per accident PD: $10,000 per accident PIP: $10,000 per person |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $15,000 per accident |

|

|

BI: $25,000 bodily injury liability per person BI: $50,000 bodily injury liability per accident PD: $20,000 property damage liability per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $20,000 per person BI: $40,000 per accident PD: $15,000 per accident |

|

|

BI: $25,000 person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident

PIP per person: $4,500 for medical expenses $900 per month to a year of disability or loss of income coverage $25 a day for in-home services $4,500 for rehabilitation-related expenses $2,000 for funeral, burial, or cremation expenses

Other: Survivor benefits of up to $900 per month up to a year for disability or loss of income and $25 per day for in-home services |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident PIP: $10,000 per person |

|

|

BI: $15,000 per person BI: $30,000 per accident PD: $25,000 per accident |

|

|

BI: $50,000 per person BI: $100,000 per accident PD: $25,000 per accident UM/UIM BI: $50,000 per person UM/UIM BI: $100,000 per accident MedPay: $2,000 |

|

|

BI: $30,000 per person BI: $60,000 per accident PD: $15,000 per accident UM/UIM BI: $30,000 per person UM/UIM BI: $60,000 per accident |

|

|

BI: $20,000 per person BI: $40,000 per accident PD: $5,000 per accident UM/UIM BI: $20,000 per person UM/UIM BI: $40,000 per accident PIP: $8,000 per accident |

|

|

BI: $20,000 per person BI: $40,000 per accident PIP: Unlimited Property protection: $1 million |

|

|

BI: $30,000 per person BI: $60,000 per accident PD: $10,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident PIP: $40,000 per person |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $20,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $20,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident UM/UIM PD: $25,000 MedPay: $1,000

Car insurance is not mandatory, but these are the requirements for those who opt in. |

|

|

PD: $5,000 per accident PIP: $1,000 per person |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $10,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $10,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident PIP: $50,000 personal injury protection per person

Other: $50,000 liability for death per person $100,000 liability for death per accident |

|

|

BI: $30,000 per person BI: $60,000 per accident PD: $25,000 per accident UM/UIM BI: $30,000 per person UM/UIM BI: $60,000 per accident UM/UIM PD: $25,000 |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident PIP: $30,000 per person |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $20,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident PIP: $15,000 per person |

|

|

BI: $15,000 per person BI: $30,000 per accident PD: $5,000 per accident MedPay: $5,000 |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $15,000 per accident |

|

|

BI: $30,000 per person BI: $60,000 per accident PD: $25,000 per accident |

|

|

BI: $25,000 per person BI: $65,000 per accident PD: $15,000 per accident PIP: $3,000 per person |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $10,000 property damage liability per accident UM/UIM BI: $50,000 per person UM/UIM BI: $100,000 per accident UM/UIM PD: $10,000 |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $20,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident UM/UIM PD: $20,000

Car insurance is not mandatory, but these are the requirements for those who opt in. |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $10,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $25,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident UM/UIM PD: $25,000 |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $10,000 per accident UM/UIM BI: $25,000 per person UM/UIM BI: $50,000 per accident |

|

|

BI: $25,000 per person BI: $50,000 per accident PD: $20,000 per accident |

|

Learn more about how car insurance works in this guide.

Motorcycle insurance is a legal requirement for anyone riding their two-wheelers on the road. Just like auto insurance, motorcycle insurance is required by law in nearly all states. The only exception is Florida.

This type of policy protects riders against financial liability if their motorcycles are involved in an accident. It also covers the repair or replacement costs if their motorbikes are damaged or stolen.

The minimum requirement for motorbike riders is liability coverage. This type of policy compensates a third party for injuries and property damage that the policyholder causes.

Other policies, including collision, PIP, UM/UIM, and guest passenger liability coverage, are available but these are optional.

A motorcycle insurance policy is also subject to minimum liability limits, which vary depending on the state. The limits are mostly similar to those in car insurance.

Find out more about how motorcycle insurance works in this comprehensive guide to bike insurance in the US.

Workers’ compensation is a type of business insurance that covers the cost of medical care and part of an employee’s lost income if they get sick or injured while doing their job.

All states, except Texas, require employers with a certain number of employees to take out coverage. Each state has its own Workers’ Compensation Board tasked with processing claims. If needed, the board also determines whether the benefits should be paid and by how much. For every successful claim, employees are given the option to receive a one-time payout or structured weekly or bi-weekly cash benefits from their employers’ insurers.

Each state implements its own regulations when it comes to workers’ compensation. You can click on the links below if you want to learn more about the laws governing workers’ compensation in your state.

|

STATE-BY-STATE GUIDE TO WORKERS’ COMPENSATION LAWS |

|||

|

|

|||

Some types of businesses, however, may be exempted from taking out workers’ compensation coverage. These include:

Sole proprietors and partnerships are given the option to self-insure. This is unless they have employees who aren’t part of the ownership.

While independent contractors aren’t legally considered employees, workers’ compensation laws in many states treat contractors, subcontractors, and their staff as employees. This means that businesses can be held liable if the contractors become injured or sick while working for them.

To avoid liability, many businesses require independent contractors to have workers’ compensation coverage before agreeing to work with them.

Learn more about how workers’ compensation insurance works in this guide.

Professional indemnity insurance protects businesses against claims resulting from alleged or actual negligence while fulfilling a professional service. Depending on the industry, this essential form of business insurance is called by different names:

Professional indemnity insurance pays for legal and settlement costs resulting from service-related mistakes and oversights, including:

Professional liability insurance covers the business and all its staff.

Businesses in certain industries are required, either by law or industry standards, to have professional indemnity insurance. Some clients may also require a professional or a company to have this type of coverage before agreeing to do business.

Here are some occupations where professional liability insurance is required by law:

Medical practitioners are legally required to carry medical malpractice insurance. These professionals include:

Medical malpractice insurance protects professionals in the medical field against claims of negligence resulting in a patient’s injury or death.

Legal malpractice insurance is required by law only in two states – Oregon and Idaho. Nearly half of all US states, however, are implementing some form of disclosure rules requiring lawyers to notify clients whether they have coverage or not.

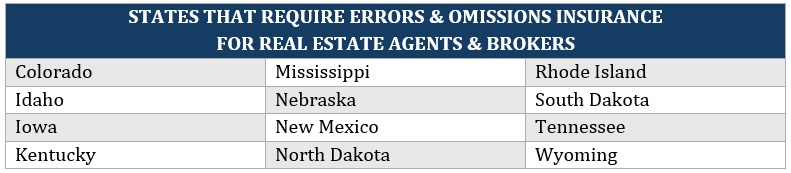

Errors and omissions insurance is compulsory for real estate professionals in several states:

The minimum coverage requirements vary between states. In Colorado and Nebraska, real estate agents and brokers must get a policy with a minimum annual aggregate limit of $300,000. In Iowa and Mississippi, the minimum limit is set at $100,000.

Some states also require insurance agents and brokers to have E&O coverage. Like real estate professionals, each state imposes different requirements. In Rhode Island, insurance sales professionals need coverage with a minimum aggregate policy limit of $500,000. In Tennessee, the minimum limit is $100,000.

The Federal Acquisition Regulation (FAR) requires businesses working on government projects to purchase professional liability insurance. According to the regulation, this type of coverage serves to protect businesses against “the perils to which the contractor is exposed.” These businesses include:

Find out more about how professional indemnity insurance works in this guide.

Health insurance is designed to help policyholders offset the high costs of medical treatment by covering a part or the entire healthcare and hospital expenses.

Passed in 2010, the Affordable Care Act (ACA), also known as Obamacare, mandated that nearly all Americans have health insurance. One of the key parts of the legislation was the individual shared responsibility provision, more popularly known as individual mandate.

Under the provision, all eligible American citizens and permanent residents must have basic health insurance, also referred to as minimum essential coverage or MEC. This provision was the closest the US came to requiring universal health coverage.

From 2014 to 2019, uninsured individuals were subject to tax penalties from the Internal Revenue Service (IRS). These penalties added up to $695 per uninsured adult or 2.5% of a person’s income, whichever was higher.

Congress repealed the mandatory penalties at a federal level in 2017. Although technically, health insurance is still required by law, uninsured individuals no longer face fines. This updated law took effect in 2019, making the individual mandate irrelevant.

Some states, however, enacted their versions of the individual mandate, which includes tax penalties. These states are:

Vermont has its own individual mandate but doesn’t impose penalties for those who fail to maintain health insurance coverage.

Here’s a summary of what insurance is required by law in the US.

Get more news and information about the latest legislative changes with the industry by visiting our Insurance News Section. Don’t forget to bookmark this page to easily access breaking news and the latest industry developments.

Is there any type of insurance that you think should be required by law in the US, but isn’t? Let us know in the comments.