Nursing homes can be a good option for seniors who need round-the-clock medical care. These facilities are mostly designed for older adults who don’t require hospitalization but can’t be cared for at home.

The high cost of nursing home care services, however, can easily deplete your personal funds. To protect your savings, you need the right coverage. But what are your options when it comes to insurance for nursing home care?

Insurance Business answers this question and more in this client education series. Whether you’re planning for your own care or helping an older loved one, this guide can prove useful.

We also encourage insurance professionals to share this piece with their clients who may be working out the right coverage for their care needs.

Learn more about the various insurance options for nursing home care in this article.

Nursing homes are designed to provide medical and personal care services for anyone, regardless of their age, who needs round-the-clock assistance. These facilities don’t cater exclusively to seniors.

Nursing homes have medical staff on hand 24/7 to provide assistance to whoever needs it. Some facilities are set up like hospitals with nurse stations on each floor. They may also come with special units for patients with debilitating illnesses such as Alzheimer’s disease, dementia, and schizophrenia.

Others are designed more like homes where residents can move freely. Some facilities allow couples to live together. Employees are also encouraged to build relationships with the residents.

The types of services nursing homes provide vary depending on the facility, but typically include:

Nursing homes, also referred to as skilled nursing facilities, are different from assisted living facilities. The latter are residential communities catering mostly to healthy and active seniors who need minimal support for daily living activities.

You can find out more about assisted living facilities and if Medicare covers the services they offer in this guide.

According to Genworth’s cost of care survey, the cost of nursing home care services are as follows:

The services and amenities that nursing homes offer vary, which dictate how much you will pay. Where the nursing facilities are located also has an impact on the cost.

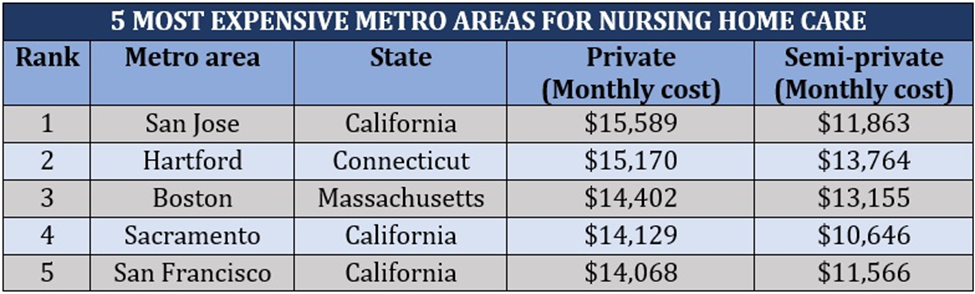

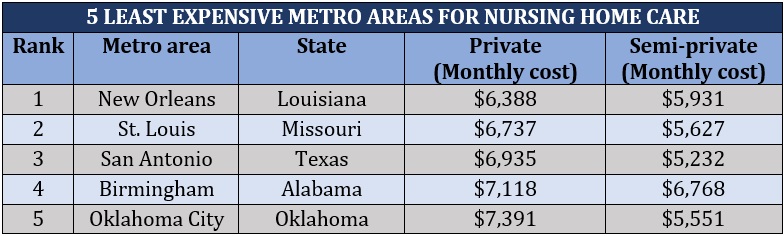

Here are the five most and least expensive metro areas for nursing home care, according to Genworth’s data. The cities are ranked based on the average monthly cost of private accommodation.

Insurance of nursing home care – most expensive metro areas

Insurance of nursing home care – least expensive metro areas

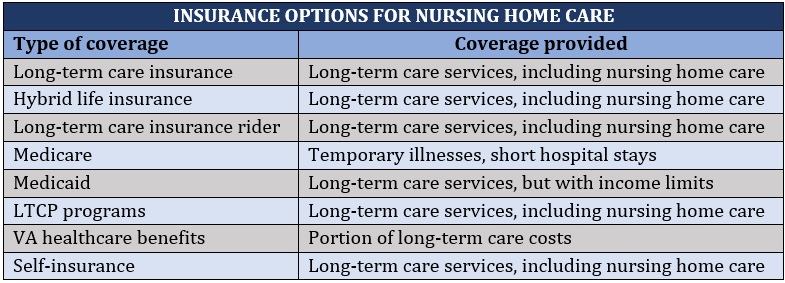

As you may have noticed in the figures above, nursing home care services can leave quite a dent in your savings. But you have several options to reduce or even cover the entire cost:

A long-term care policy is a good option if you’re looking for insurance for nursing home care services.

Sometimes referred to as extended care insurance, it pays for the cost of medical and non-medical services for those who have lost the ability to care for themselves.

Long-term care insurance covers care provided in nursing homes, assisted living facilities, adult day care centers, and at home. Some policies also provide coverage for those suffering from debilitating conditions, including dementia, multiple sclerosis, and Alzheimer’s disease.

State requirements vary for those who can access coverage. But generally, you will need certification from a reputable healthcare provider stating that you no longer perform at least 2 of the 6 ADLs. These are eating, bathing, dressing, toileting, transferring, and continence.

Learn more about how long-term care insurance works in this comprehensive guide.

Some insurers allow you to pair your life insurance plan with an annuity or long-term care insurance policy. Also referred to as a linked benefits or hybrid policy, this type of plan provides separate cover for your long-term care needs, eliminating the need to tap into your death benefit.

Krystie Dascoli, voluntary benefits practice leader at Marsh McLennan Agency, recommends taking out a hybrid policy over a standard long-term care plan because of these benefits.

“Standalone or traditional long-term care insurance is a ‘use it or lose it’ type of policy,” explains Dascoli, who is also a certified voluntary benefits specialist (CVBS). “An individual who purchases a standalone long-term care policy has a 50/50 chance of using it. An insured could hold on to this type of policy for many years and never use it.

“On the other hand, a hybrid life insurance policy is a multi-use policy that not only pays a death benefit but can also pay when a person is diagnosed with a terminal illness or when the individual needs long-term care. We promote the hybrid policies more because, at some point, the individual will use it and it also builds cash value.”

If you already have a life insurance plan, you may be able to purchase a rider to cover long-term care costs. This add-on allows you to use part of your death benefit to pay for long-term care services such as those provided in nursing homes.

Life insurance, however, comes in different structures, so it would be best to consult an experienced life insurance agent or broker to know if you’re eligible to purchase this rider. You can also check out this guide to learn more about how life insurance works.

Medicare is a government-sponsored health insurance program available to seniors and younger people with certain disabilities. It is also accessible to those with end-stage renal disease (ESRD) or permanent kidney failure that requires dialysis or a transplant.

Medicare, however, offers limited benefits for nursing home stays following hospitalization, covering only temporary or acute illnesses. Medicare doesn’t pay for long-term custodial care or chronic medical conditions.

Medicaid is another government-funded program, but unlike Medicare, it provides financial support for long-term medical conditions. The program, however, comes with strict eligibility requirements, which vary depending on the state.

There are 38 states that allow income to be the sole basis of qualification. The cutoff is usually 138% of the federal poverty level (FPL).

A larger household means a higher income limit. Some beneficiaries may also need to liquidate their assets or spend a portion of their benefits out of pocket through the Medicaid spend-down program to qualify.

Medicaid and Medicare are often confused with each other because of the programs’ similar-sounding names. It doesn’t help that in certain situations, people may be eligible for both.

If you want to understand more about the key differences of these government-administered programs, you can check out our comprehensive guide to affordable health insurance.

Most states run a long-term care partnership program, which is a collaboration between private long-term care insurance providers and the state’s Medicaid program. The goal of these partnerships is to encourage people to purchase long-term care policies and reduce the state’s burden of shouldering care services through Medicaid.

The main benefit of joining LTCP programs is that it allows you to protect your assets from Medicaid’s income limits. This means that you don’t have to spend almost all your savings just to qualify for Medicaid.

Some states with active long-term care partnership programs include Arizona, California, Connecticut, Indiana, and New York.

If you’re a military veteran or a surviving spouse, you may be eligible for long-term care assistance, including nursing home care, through the Department of Veteran Affairs (VA). To qualify, you must be enrolled in a VA healthcare benefits program.

Under the program, the VA determines what long-term care services you need. Depending on the type of care, you may be required to shoulder part of the costs.

If you feel that you have sufficient funds to cover nursing home care costs when the need arises, then paying for the services out of pocket may be a good idea. The biggest benefit of self-insurance is that you can allocate the money you would’ve otherwise spent on premiums to other expenses.

Here’s a summary of the different options you have when it comes to insurance for nursing home care.

The amount you pay for nursing home care coverage depends on the type of insurance you take out.

According to the latest price index from the American Association for Long-Term Care Insurance (AALTCI), premiums for long-term care insurance range from $900 to $9,575. Among the factors that impact pricing are a person’s age, marital status, health condition, and policy features.

Check out this guide to understand the math behind the cost of long-term care insurance.

Just like in long-term care insurance, the premiums for life insurance plans are influenced by a range of personal factors. This is why it’s difficult to provide a one-size-fits-all estimate. The death benefit amount is one of the biggest factors that affect rates. Purchasing a long-term care insurance rider will raise the cost further.

Hybrid policies cost even more because of the unique benefits they provide. To save on premiums, Dascoli recommends taking out coverage while you’re young.

“The only real downside to either of these policies is that premiums can be steep, especially the older an individual gets,” she notes. “It is important to purchase a hybrid policy at a young age to offer the most financial protection long-term.”

Once you turn 65 years old, there’s nearly a 70% chance that you will eventually need long-term care support. This is according to data gathered by the Administration for Community Living (ACL).

The ACL’s research also reveals that women typically need care services for an average of 3.7 years, while men need it for around 2.2 years. A quarter of older adults, regardless of their gender, will also require care support for more than five years.

Without proper coverage, you’ll have to pay for such expenses, which include nursing home care, out of pocket. Unfortunately, the high cost of these services can easily eat into your personal funds.

While you can access financial assistance through Medicaid, your choices are often limited to nursing home facilities that accept payments from the program. Medicaid also imposes strict income limits, which may require you to spend yourself into poverty. Despite this, it still won’t cover all your nursing home care costs.

Getting the right type of coverage gives you more options for accessing the best nursing home care services possible.

Find out what the experts say about the best time to take out coverage in our guide to long-term care insurance cost by age.

Do you think getting insurance for nursing home care is necessary? What types of policies do you think offer the best protection? Share your thoughts below.