Getting an insurance business up and running often requires heavy financing – but how much funding do you really need?

To give you an idea of the overall expenses, Insurance Business breaks down the different costs involved when launching your own insurance company. We will also explore the various ways you can secure funding and keep your business profitable.

If you’re an aspiring insurance entrepreneur but not quite sure if you can afford the startup expenses, you’ve come to the right place. Read on and find out how much it costs to start an insurance company in this guide.

Starting your own insurance company can be an expensive project. You need sufficient funding not just to sustain your daily operations but also to maintain a positive cash flow, especially in the first few years of your business.

Depending on the size and structure of the business, industry experts estimate startup capital of between $50,000 and $500,000, possibly even more. Let’s break down the different costs involved in starting your own insurance company.

One of the first and most important steps you must take if you’re planning to launch your own insurance company is getting the right licenses. Almost all businesses and professionals operating in the industry need a license to legally provide a product or service. The licensing requirements – including related fees – vary depending on the state and specialization, which have a direct impact on your startup costs.

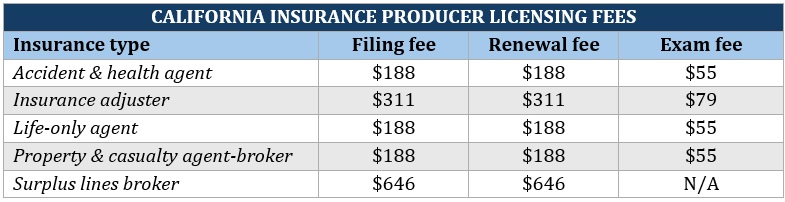

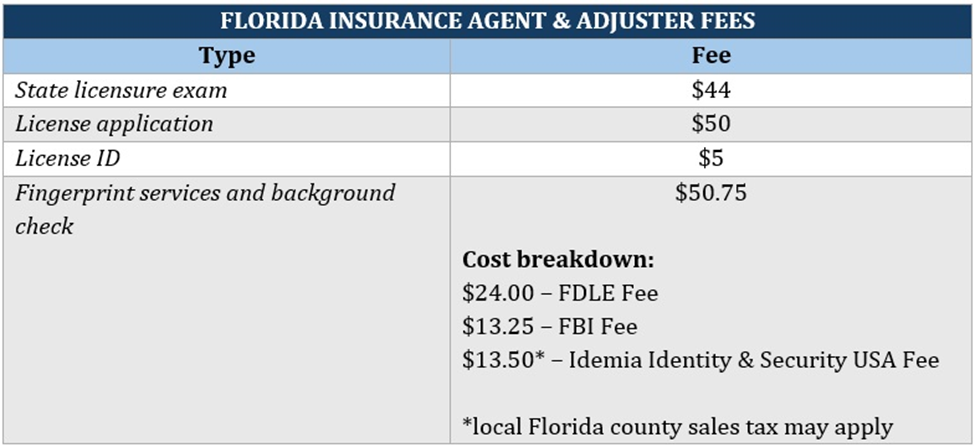

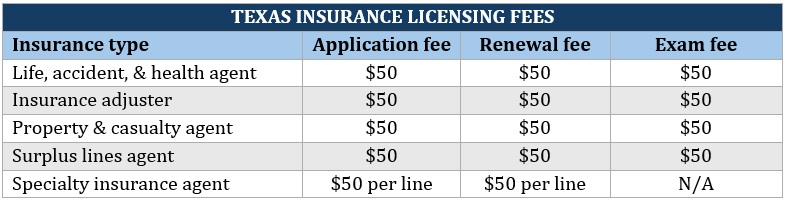

To illustrate, we will break down the costs of obtaining an insurance license in California, Florida, and Texas.

If you want to start an insurance company in the Golden State, this guide on how to get a California insurance agency license can help.

For more information on what licenses you need to launch an insurance business in the Sunshine State, check out this guide to insurance agency licenses in Florida.

Here’s how you can get a Texas insurance agency license if you plan on running your insurance business in the state.

Apart from industry licenses, you may need to secure the necessary business licenses and permits for your insurance company to legally operate. Just like insurance agency licenses, the requirements for getting a business license vary depending on the state.

Here’s a list of business registration and licensing requirements, along with the estimated costs, that you may need to meet to start an insurance company.

Insurance companies are required to register as a “resident business entity” through their state insurance commissioner’s office. Because each jurisdiction has different requirements, it’s difficult to provide a single estimate of how much state registration fees cost.

To make the process easier, the National Association of Insurance Commissioners (NAIC), has created a portal where you can file your uniform certificate of authority application (UCAA). You can contact the corresponding agency in your state to find out the requirements and how much registration costs. NAIC charges a usage fee of $30 for domestic filings.

Business registration

You will need to register the name of your insurance company. Some states prohibit or restrict the use of certain terms to avoid misleading the public. Among the information you need to provide to register your business are:

It may cost you around $300 to register your insurance company.

Depending on your location, you may need to secure general business permits or licenses for your insurance business. These may include:

This step-by-step guide on how to start an insurance company can give you a rundown of the different business registration and licensing requirements.

Once you get your business up and running, you will need funding for your daily operational expenses. Here’s a breakdown of the estimated operational costs when starting an insurance company.

The cost of renting an office space for your business depends on a range of factors, including:

Office spaces are also categorized into classes, which are based on amenities, location, and overall quality. Here’s a breakdown of how much it costs to rent an office space based on these classes, according to this industry website.

|

OFFICE SPACE RENTAL COSTS BY CLASS |

||

|

Class |

What it means |

Average cost per square foot |

|

Class A |

Prime location, state-of-the-art facilities, professional management |

$30 to $60 |

|

Class B |

Decent location with reasonable amenities |

$20 to $35 |

|

Class C |

Affordable location, fewer amenities, may require maintenance or renovation |

$10 to $20 |

Source: ACRE Real Estate Partners

Having the right equipment plays an important role in helping your insurance business succeed. Equipment-wise, each employee should have access to:

A 2014 study by OPI.net has found that small companies paid the highest to keep their offices supplied. Here’s a breakdown of the costs. Since the estimates are a bit old, the Insurance Business research team adjusted the numbers to account for inflation.

Cost to start an insurance company – office equipment and supplies

|

OFFICE SUPPLIES & EQUIPMENT ESTIMATED SPEND |

||

|

Business size |

Monthly cost per employee (2014) |

Monthly cost per employee (inflation adjusted) |

|

1 to 4 employees |

$77 to $92 |

$102 to $122 |

|

40 employees |

$45 to $53 |

$60 to $70 |

|

200+ employees |

$27 to $32 |

$36 to $42 |

Even if you’re running your business remotely, you will still need to invest in quality equipment. This article shows you how to start an insurance agency from home.

You may choose to operate your insurance company on your own or employ staff. If you choose to hire employees, you’re legally required to provide compensation, including:

Insurance companies on average spend between 50% and 75% of their revenue on employee compensation. This is an insurance business’ single largest expense.

Effective marketing is one of the keys to attracting and retaining clients. Insurance companies typically spend between 1% and 10% of revenue on advertising. Since your business is new, you can find affordable ways to build your customer network. These include building a user-friendly website and establishing a professional social media presence.

Here are some more networking tips to help your insurance business grow.

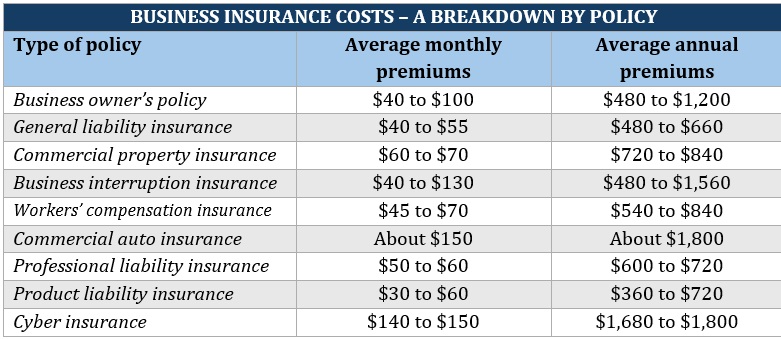

Wouldn’t it be ironic if your insurance company operated without the necessary coverage? Having the right business insurance policies can go a long way to keeping your insurance firm financially protected. Here’s a breakdown of how much premiums for the different coverages cost.

Learn more about the different types of business insurance your insurance company may need in this guide.

You can use your personal funds to cover the cost of starting an insurance company. These may include money from your personal savings or an amount you raise by selling properties or other assets. But if your personal funds still aren’t enough, there are other ways for you to secure financing to launch your insurance business. These include:

This is the most common way of raising capital for a startup business. You can apply for a business loan through banks and other lenders. A solid business plan and a good credit history are often required to get approval.

The Small Business Administration can act as a guarantor to help you secure bank approval through an SBA-guaranteed loan.

The federal government has several financial assistance programs to help fund new businesses. You can visit grants.gov to look for grants to help you start your own insurance company.

Crowdfunding websites offer a low-risk option if you’re searching for donors to finance your insurance business.

The continued growth of the insurance industry presents a big opportunity for business owners who want to start their own insurance company. Insurance products and services remain in high demand as people are always in need of financial protection.

Just like any type of business, running an insurance business requires careful planning and preparation. To keep customers coming and the cash flow running, you must have a clear vision of how to maintain your business’ profitability. Here are some ways for your insurance company to sustain revenue growth.

Having clear goals gives your insurance company a picture of where it wants to go. You should also have a plan in place for how to reach these targets. If set correctly, these goals can help you measure the success of your insurance business.

To succeed in the insurance market, you need to drive leads continuously. This is the lifeline of your business in a highly competitive industry.

Clients’ needs evolve constantly, pushing demand for different insurance products. This gives your business an opportunity to find a niche that will help it grow. This can take a lot of time and effort but can reap dividends in the long run.

The insurance industry is increasingly embracing technology to move forward. This is evident in advanced technology such as AI, telematics, blockchain, and cloud computing. Take advantage of these technological innovations to help your insurance company reduce costs, mitigate risks, and attract and retain customers.

Don’t forget to take care of your insurance company’s most important asset – your employees. A great insurance employer provides the best work environment for staff to thrive and grow. A positive workplace culture also contributes to an engaged workforce, which is key to boosting productivity and maintaining profitability.

Would you like a little more hepl starting your insurance company? Have you thought about franchising? Check out our guide to starting a State Farm insurance agency.

Do you think you’re ready to start an insurance company? Share your plans in the comments