One of the biggest drawbacks of long-term care insurance is it doesn’t come cheap. But depending on your age, you may be able to access lower premiums.

In this part of our client education series, Insurance Business gives you a breakdown of long-term care insurance cost by age. We also talked to industry experts who will explain when the best time is to purchase coverage.

If you’re planning for your own care or helping an older loved one, this guide can provide an overview of how much coverage costs.

If you’re an insurance professional, share this piece with your clients to help them make informed purchasing decisions.

Read on and find the answers to the most pressing questions about long-term care insurance costs.

Your age is one of the biggest factors that influence how much premiums cost for a long-term care insurance policy. Generally, you can access lower rates if you purchase a policy in your working years, although you may have to pay for the plan longer.

Industry non-profit American Association for Long Term Care Insurance (AALTCI) has released its latest price index. This details how much policyholders can expect to pay in yearly premiums.

Here’s a summary of long-term care insurance cost by age, gender, and marital status for policies worth $165,000. This also includes premium estimates for policies with inflation growth provisions.

|

Buyer |

Level benefits |

Benefits growing at 1% yearly |

Benefits growing at 2% yearly |

Benefits growing at 3% yearly |

Benefits growing at 5% yearly |

|

Single male |

$950 |

$1,375 |

$1,750 |

$2,220 |

$3,685 |

|

Single female |

$1,500 |

$2,150 |

$2,815 |

$3,700 |

$6,400 |

|

Married couple |

$2,080 combined |

$3,000 combined |

$3,870 combined |

$5,025 combined |

$8,575 combined |

According to AALTCI’s price index, the value of this policy can increase to $222,400 once the policyholder reaches 85 years old for plans with a 1% inflation growth provision. For those with a 2% provision, the policy can be worth $298,900 and $400,500 for policies with a 3% growth benefit.

|

Buyer |

Level benefits |

Benefits growing at 1% yearly |

Benefits growing at 2% yearly |

Benefits growing at 3% yearly |

Benefits growing at 5% yearly |

|

Single male |

$1,175 |

$1,600 |

$2,000 |

$2,525 |

$3,800 |

|

Single female |

$1,900 |

$2,550 |

$3,300 |

$4,300 |

$6,600 |

|

Married couple |

$2,600 combined |

$3,525 combined |

$4,525 combined |

$5,800 combined |

$8,750 combined |

This long-term care insurance policy can be worth $211,600 once the policyholder turns 85 if the plan has a 1% inflation growth provision. The value increases to $270,700, $345,500, and $588,750 for policies with 2%, 3% and 5% inflation benefits, respectively.

|

Buyer |

Level benefits |

Benefits growing at 1% yearly |

Benefits growing at 2% yearly |

Benefits growing at 3% yearly |

Benefits growing at 5% yearly |

|

Single male |

$1,700 |

$2,165 |

$2,600 |

$3,135 |

$4,200 |

|

Single female |

$2,700 |

$3,400 |

$4,230 |

$5,265 |

$7,225 |

|

Married couple |

$3,750 combined |

$4,735 combined |

$5,815 combined |

$7,150 combined |

$7,150 combined |

For this type of policy, those with 1% inflation growth provisions can be valued at $201,300 after the policyholder’s 85th birthday. Plans can be valued at $245,000, $298,500, and $437,800 if they have growth benefits of 2%, 3%, and 5%, respectively.

The premiums above are for “Select” long-term care insurance policies, which are more expensive than “Preferred” plans, according to the AALTCI. The group also notes that the rates are for Illinois clients. Your long-term care insurance cost can be higher or lower, depending on several factors, including your residence.

For a more detailed discussion on how much long-term care insurance costs, you can check out this guide.

Industry experts recommend purchasing long-term care insurance while you’re young. Taking out coverage at a younger age can help lower your premiums, although you will also need to make payments longer.

The American Association of Retired Persons (AARP) describes your early to mid-60s as the “sweet spot” if you’re single. If you’re married, the group suggests that the best time to take out coverage, along with your spouse, is at the age of 55.

AARP notes that long-term care insurance costs may be higher at this age range than if you buy coverage in your late 40s to early 50s, but you’ll pay less premiums overall until you reach 80 years old.

Krystie Dascoli, voluntary benefits practice leader at Marsh McLennan Agency, recommends getting coverage while you’re still gainfully employed.

“Rates will go up significantly with age, so buying a long-term care policy early in the working years is ideal,” explains Dascoli, who is also a certified voluntary benefits specialist (CVBS).

“Whether an individual purchases individual long-term care or a hybrid life insurance policy with a long-term care rider, the best age to buy is as soon as possible. These programs are rated at issue age and never go up. So, if someone buys a policy at age 25 and the rate is $35 per month, they will pay $35 for as long as they own the policy.”

If you reach 65 years old and still haven’t purchased a long-term care insurance policy, taking out coverage “should still be a consideration,” according to Dascoli.

“A big mistake we see individuals make is waiting until after retirement to purchase long-term care insurance,” she explains. “By purchasing long-term care plans during their working years and through their employer, individuals will have the opportunity to buy this insurance without answering medical questions and usually have access to higher face amounts. This is especially important for anyone with pre-existing medical conditions.”

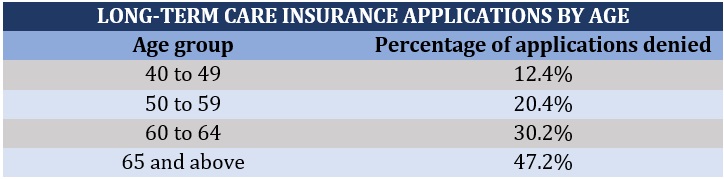

The AALTCI’s data, meanwhile, reveals how the age at which you apply for coverage can impact your eligibility.

Based on these figures, you can see how your chances of qualifying for coverage decrease as you get older. If you already need assistance with daily activities or have a chronic or debilitating illness, your long-term care insurance application will likely be denied.

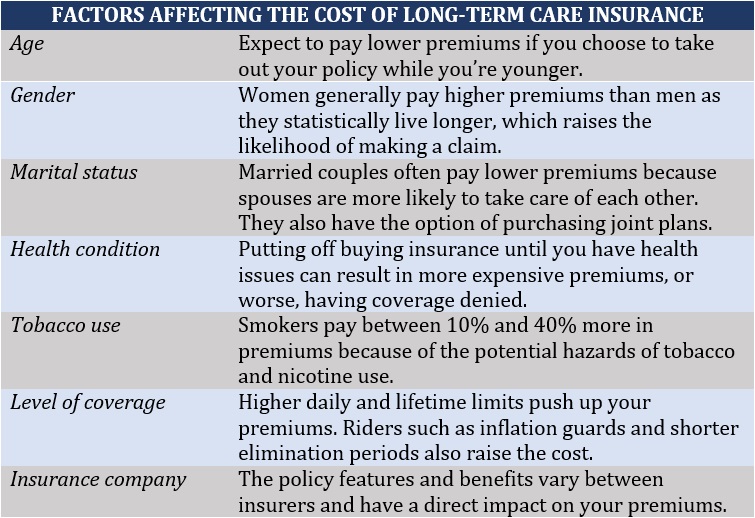

Apart from your age, there are several other factors that impact the cost of long-term care insurance. Here’s a summary:

A standard long-term care insurance policy pays for the cost of medical and non-medical services for those who have lost the ability to care for themselves. This type of care can be accessed at home, or in assisted living facilities, nursing homes, or adult day care centers.

The eligibility criteria for accessing benefits under standalone long-term care insurance vary between states. But generally, you will need certification from a healthcare provider stating that you need “substantial assistance” in performing at least two of these six activities for daily living:

Some policies may also provide coverage if you suffer from a debilitating condition, including Alzheimer’s disease or dementia.

Most standard long-term care insurance plans require you to pay for the cost of services yourself for a specific timeframe, also referred to as the waiting or elimination period. This lasts 30 to 90 days before your insurer reimburses the costs. Coverage comes with a daily limit and pays out until your policy reaches its lifetime maximum.

But there’s another type of long-term care insurance, called a hybrid policy, that comes with the features of a life insurance policy or a qualifying annuity.

Hybrid long-term care insurance policies provide a death benefit if you don’t get to use the long-term care payouts. The premiums for this type of coverage are often more expensive but are guaranteed to remain the same over the life of the policy.

Just like whole life insurance, hybrid plans allow you to receive a cash value if you decide to surrender the policy. Some policies provide a partial refund of the premiums you’ve paid.

“An individual who purchases a standalone long-term care policy has a 50/50 chance of using it,” explains Dascoli. “Standalone or traditional long-term care insurance is a 'use it or lose it' type of policy. An insured could hold on to this type of policy for many years and never use it.

“A hybrid life insurance policy, on the other hand, is a multi-use policy that not only pays a death benefit but can also pay when a person is diagnosed with a terminal illness or when the individual needs long-term care. We promote the hybrid policies more because, at some point, the individual will use it and it also builds cash value.”

To find the best long-term care insurance policy for your needs, there are several factors that you need to consider, including:

Assess the type of care you expect to receive and how much it costs on a daily basis. Long-term care insurance costs vary greatly depending on the quality of care and where you plan to access it.

Some insurers will give you the option to choose how long you want to pay for the policy, usually ranging from two years to a lifetime. When deciding on your policy’s term length, you should factor in your medical history. If you have a family history of a debilitating illness that requires many years of care, it may be advisable to choose a longer benefit period.

This is the period when you’re required to pay for care services out of pocket before your insurer reimburses the costs. You can often choose between 30, 60, and 90 days. The longer the elimination period, the lower your premiums are.

Inflation causes medical expenses to soar. That’s why many long-term care insurance providers offer a rider to protect against inflation. This add-on can increase the value of your daily benefit every year but at an extra cost.

Most insurers offer tax-qualified policies that come with tax-free benefits and deductible premiums. The deductions vary depending on the taxpayer’s age.

Here are the latest deduction limits based on the data gathered by AALTCI.

|

Attained age before close of taxable year |

2023 limits |

2022 limits |

|

40 and under |

$480 |

$450 |

|

Over 40 but under 50 |

$890 |

$850 |

|

Over 50 but under 60 |

$1,790 |

$1,690 |

|

Over 60 but under 70 |

$4,770 |

$4,510 |

|

Over 70 |

$5,960 |

$5,640 |

With many providers exiting the market in recent years, it’s important to practice due diligence when choosing an insurer. Go with a company that is both financially stable and committed to offering clients the best care possible.

Our comprehensive guide to extended care insurance provides more information on how you can find the best coverage for your long-term care needs.

Americans have a roughly 70% chance of needing long-term care services after turning 65, according to the latest estimates from the Administration for Community Living (ACL). The agency is a branch of the US Department of Health and Human Services (DHHS).

Data that ACL gathered also shows that women need long-term care support for an average of 3.7 years, while men will require it for 2.2 years. A quarter of all seniors, regardless of their gender, may also need care services for at least five years.

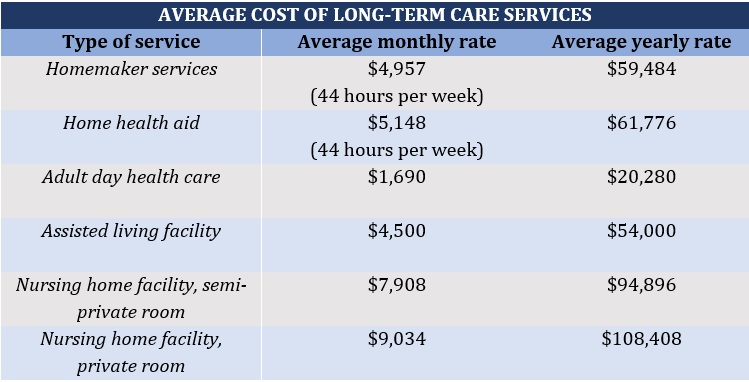

Without long-term care insurance, you’ll have to pay for these expenses yourself – and they can prove costly. To give you an idea of how much care services cost, here’s a summary from Genworth’s latest cost of care survey.

Given the costs, long-term care services can deplete your retirement funds very quickly. Long-term care insurance can help protect your retirement savings.

And while you can get assistance through Medicaid, your choices are often limited to nursing homes that accept payments from the government-sponsored program. You can also access Medicaid only if you’ve exhausted most of your savings. Despite this, Medicaid won’t cover all your assisted living costs.

But one of the biggest misconceptions about long-term care insurance is that it caters exclusively to seniors who need assistance due to age-related impairments. The fact is people of all ages can develop conditions or get into accidents that may require them to access assistance with daily activities. This shows that the need for long-term care insurance spans across age groups.

“Long-term care can happen at any time in someone’s life, not just due to old age or chronic illness,” Dascoli notes. “This is a great program to complement other financial wellness programs such as term life and disability insurance.”

If you want to learn more about the benefits of this type of coverage, you can check out our comprehensive guide to long-term care insurance.

What do you think about the long-term care insurance cost by age? Do you agree with our experts’ opinion on the best age to purchase coverage? Share your thoughts below.