The Financial Markets Authority (FMA) – Te Mana Tātai Hokohoko – has initiated a broad review of how financial advice is accessed and delivered across New Zealand, aiming to identify barriers and support sector-wide improvements.

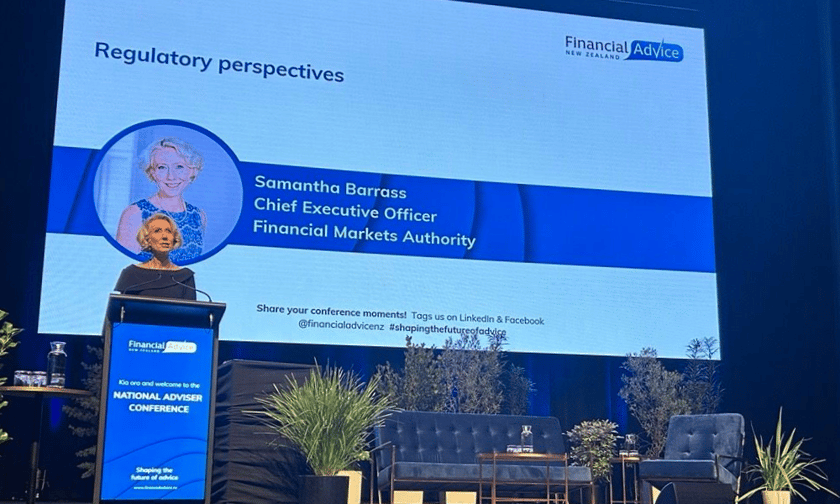

The announcement was made by chief executive Samantha Barrass (pictured) during her address at the Financial Advice New Zealand (FANZ) conference held in Christchurch.

The regulator’s review will explore structural and operational factors influencing the availability of advice to consumers, with a specific focus on:

According to the FMA, the exercise is intended to guide future regulatory priorities and reduce any unnecessary constraints that could limit the sector’s ability to serve New Zealanders effectively.

Barrass stated the FMA is aiming to better understand how regulatory oversight can support broader access to sound advice.

“We know there are many positive impacts on consumers who receive good quality financial advice. This is about understanding how we as a regulator continue to ensure we regulate in a way that ensures quality advice [reaches] even more New Zealanders,” she said.

The review will gather industry and stakeholder input to help determine areas where the regulatory framework can be refined.

A consultation period on the draft terms of reference is now open and will close on May 30.

EMBED

<iframe src="https://www.linkedin.com/embed/feed/update/urn:li:share:7313015489767620608?collapsed=1" height="399" width="504" frameborder="0" allowfullscreen="" title="Embedded post"></iframe>

FANZ chief executive Nick Hakes expressed support for the initiative, noting the opportunity for the advice sector to contribute.

“I would like to thank Ms Barrass and the FMA’s financial advice team for the opportunity to collaborate on the draft terms of reference of the review. We encourage everyone to have their say on how they think the review can best serve financial advice providers and New Zealanders,” he said.

Alongside the review, the FMA is also initiating a more detailed examination of business models used by licensed financial advice providers (FAPs). This effort aims to support more targeted regulatory conversations around fairness, suitability, and conduct risk.

This initiative comes after the FMA released an overview of the financial advice sector’s regulatory returns for the year ending June 30, 2024.

The data, collected from 1,410 licensed FAPs, showed that 8,472 financial advisers were active in the market, down from 9,300 in 2021. Advice related to life and health insurance remained the most commonly offered services. According to the data, 36 providers offered digital advice platforms, serving approximately 86,500 clients.

The FMA noted that 97% of complaints received were resolved within three months, and many providers operate across multiple product areas or through referral networks.

Barrass said that understanding how advice businesses operate will allow the FMA to engage more effectively and anticipate potential conduct issues.

“Analysing business models is critical to helping the FMA identify emerging risks around firms treating clients fairly, providing suitable advice, and operating with integrity. It will make our regulatory approach real by shifting to having more sophisticated conversations with FAPs about how compliance fits within their business,” she said.

Separately, the CoFI regime came into force on March 31, placing new conduct obligations on licensed banks, insurers, and non-bank deposit takers.

Under the new rules, institutions must establish and maintain fair conduct programmes that guide customer interactions throughout the product lifecycle, including onboarding, servicing, and complaints handling.

Institutions are also required to publish summaries of their conduct programmes to give consumers greater transparency into how financial service providers are meeting their obligations.