Big changes are coming for the standards and definitions in New Zealand’s insurance contracts, some of which are more than 100 years old.

The Contracts of Insurance Bill is expected to become law by the end of the year and will consolidate six different acts relevant to insurance contracts into the one Bill. Among other things, the legislation will add a Duty of Utmost Good Faith to the relationship between insurers and customers.

Then, early in 2025, the Financial Markets Authority (FMA) is introducing an act that sets new standards around how insurers treat consumers. The Financial Markets (Conduct of Institutions) Amendment Act 2022 (the CoFI Act) aims to make sure banks and insurers conduct business according to a fair conduct principle.

So, how do brokers regard these changes?

Speakers at the recent New Zealand Underwriting Agencies Council (NZUAC) Expo in Auckland tackled both of these hefty regulatory changes. Michael Hewes, the FMA’s director, discussed the CoFI Act. Michael Cavanaugh (pictured below), Wotton + Kearney’s (W + K’s) special counsel, explained the changes for brokers and insurers in the upcoming Contracts of Insurance Bill.

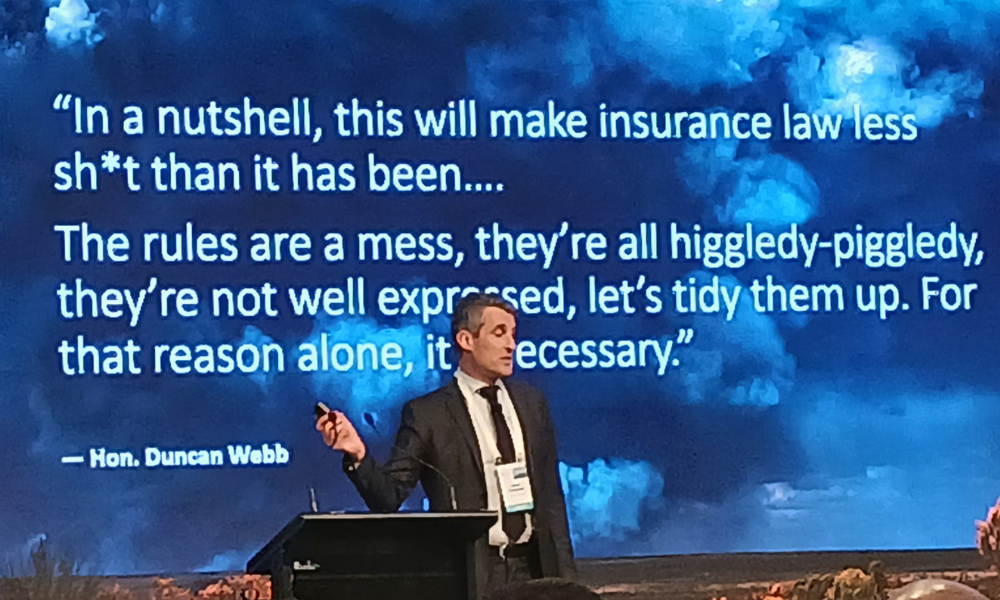

Cavanaugh summarised the impacts by quoting Duncan Webb, the current Labour MP and former Minister of Commerce and Consumer Affairs:

“In a nutshell, this will make insurance law less sh*t than it has been…”

Insurance Business attended the Expo and asked brokers about the changes.

Dall said one reason for attending the expo was to educate himself around these legislative changes that are going to affect everybody in the industry.

Dall’s colleague, Trina Rowley (main picture, right), agreed.

“The session we just were in was really interesting in terms of the legislation changes and just trying to get your head around all of that and what the implications are,” said Rowley, the firm’s executive general manager of broking services and business operations.

However, she said unlike smaller brokerages, her large firm has the advantage of a team of lawyers and risk experts.

“It’s really easy to flick it over to them and say, ‘What does this mean?’ But a lot of small brokers won’t have that luxury,” said Rowley.

She also said that previous legislation that came into force during 2020 – the Financial Services Legislation Amendment Act 2019 – already put them onto this path.

“That was a big change and adjusting to that was quite challenging - but we’ve already adjusted,” said Rowley.

She said the main thrust of these earlier changes involved two components.

“The first part was all about your code of conduct,” said Rowley. She included how the firm: operates, puts clients first, recognizes clients with vulnerabilities, makes sure clients understand any advice and treats them fairly.

“The other part was very much around disclosure,” said Rowley.

She said the main change there was probably the steps an insurance firm now needs to follow, including their timing. For example, when advice is given and when a quote is provided. Also, details around how income is earned.

“That was a real adjustment,” said Rowley. “Prior to that, we didn’t have to disclose the amount that we earned.”

Now, she said, brokers must disclose what they earn from insurers and also any fees that they add to a client’s insurance bill.

“The other part is that, as a brokering firm, we now have to be licensed - and as a person giving advice, you have to get a qualification,” said Rowley.

For the regulatory changes discussed at this Expo and currently in play, Rowley said it will be interesting to see how insurers apply them and, from there, what new requirements are placed on brokers.

Dall agreed. “Absolutely,” he said. “For me personally, this is about what is going to be expected of the broker down the line.”

Dall said educating clients about how the changes impact them will be important. “I think that’s where the connection has to be made for us, so we need to understand what’s going on,” he said.

One impact of the recent years of regulation, said Rowley, is her job takes more time, particularly around preparing what you need to give to the client.

“It’s not a bad thing because I feel like it’s put more professionalism and discipline into our industry which is good,” she said. “If you actually have a higher standard and you can lift that standard and clients get a better outcome then I think that’s a good thing.”

Did you attend the New Zealand Underwriting Agencies Council (NZUAC) Expos in either Auckland or Christchurch? What did you learn? Please tell us below.