With the issue of climate change and emission reductions moving fast, insurers will soon have to take a hard look at their investment portfolios, and Insurance Council of New Zealand chief executive Tim Grafton said we may start to see insurers adjusting those portfolios and dropping their higher-risk investments.

The government’s new climate change reporting bill means insurers will need to reassess their exposure to things like high-risk housing, and also their investments into potentially environmentally unfriendly organisations or sectors.

Grafton said we will likely see insurers increasingly ditching their investments into these spaces, and replacing them with those that will support a low-carbon economy.

“Insurers will naturally be looking to reduce their exposure in high emissions areas, not only because it makes good sense for the planet and their reputation, but also because it makes good financial sense,” Grafton said.

“Over time, every company in the world is going to need to look at their investments, and insurers will be no different.”

“Reporting on that will provide a much greater focus on identifying information that would be important for investors to know about, and requiring insurers to look five, 10, 20 or 30 years into the future provides them with an opportunity to identify the risks and opportunities that exist around their investment portfolios,” he explained.

“Clearly, that will encourage more of those firms to start adjusting those portfolios, especially where the risks to those investments are likely to increase. And where opportunities present themselves to invest elsewhere, looking at the long-term risks might help inform that.”

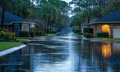

Grafton said that insurers will be also be looking at assets that are likely to significantly decrease in value over time, and the most obvious area of scrutiny will be coastal properties vulnerable to flooding.

Read more: RBNZ welcomes climate change consultation

He said that mandatory reporting will help present a clear picture of these risks, and will ultimately guide insurer decisions around the level of risk that they’re willing to take on.

“Insurers will be looking at what financial exposure they have to, say, tens of thousands of homes that may face an increased risk of flooding,” Grafton said.

“The investments that an insurer has in those kinds of assets may change significantly in value over the coming decades, and so keeping a transparent and open record that is available to regulators will be important to making an accurate verification of climate change exposure.”