Ever-escalating costs, including rapidly rising insurance premiums, are putting Wellington businesses at risk.

That was the key issue highlighted in the recently held insurance forum in the capital. Wellington Chamber of Commerce chief executive officer John Milford stressed how insurance premiums are increasing commercial rents and putting the squeeze on businesses’ fixed costs.

“Insurance premiums in Wellington rose after the Canterbury earthquakes, rose again after the Kaikoura earthquake, and are now rising yet again due to insurers adopting ‘risk-based’ pricing,” Milford said. “There appears to be no end to rising premiums.”

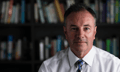

Meanwhile, Insurance Council of New Zealand (ICNZ) chief executive Tim Grafton told the forum that it was vital to take collective responsibility.

“Really though it’s about how we manage our seismic risks,” Grafton said. “That is a collective responsibility for all – government, council, regulators, banks, developers, building owners, their advisers, the insurance brokers, and insurers.”

He talked about how insurers assess risk and how New Zealand compares with similar countries. He also offered potential solutions, claiming the only way to ensure long-term affordability in a sustainable way is to reduce risk.

For example, he proposed changing building standards to increase resilience and reduce the risk of total insured loss. He also said people need to invest in retrofitting properties for resilience – including adopting low-cost remidiation techniques and installing low-cost seismic devices.

“These aren’t overnight solutions, but they are needed to keep Wellington thriving and surviving for years to come,” he said.

Grafton added that a short-term solution is to share more of the risk. He suggested giving corporates flexibility to increase their insurance excess; and to get rid of the Fire Service Levy on insurance premiums, which is uncapped for commercial property. He noted commercial property is brokered, with some brokers charging a flat-fee, others a 25-30% commission on the premium. If premiums have shot up 30% this year, is it necessary to add another 10% on top, he asked?

Grafton was critical of some options that avoid reducing risk. He suggested that having another state insurer or raising the EQC cap still means having to buy reinsurance support like private insurers do. He noted government capital is far better invested in low cost repair methods and resilient retrofits than being an alternative source for risk transfer. Additionally, he pointed out that the proposal to increase the EQC cap shifts the costs to every New Zealand homeowner. This means every Kiwi would pay more to supprt Wellington, instead of getting a relative reduction in earthquake premium from their private insurer, he said.

“Is it really the policy objective that every New Zealander is fully insured no matter how high the risk at an affordable premium?” Grafton asked the forum. “That happens nowhere else in the world, and it only ever happened because we never really understood the risk.

“For our part, we will work with our members to communicate more openly and transparently about the risks that people face,” he added.

The insurance forum was called by Wellington City Mayor Justin Lester and was attended by over 100 decision-makers, including Finance Minister Grant Robertson, Earthquake Commission (EQC) Minister Megan Woods and Commerce Minister Kris Faafoi.