Fidelity Life has announced higher non-medical limits for lump-sum covers, allowing customers to access higher cover amounts without the need for mandatory medical evidence or testing.

According to the locally owned life insurer, this move is part of a package of improved underwriting requirements which will benefit customers and advisers alike.

The new underwriting requirements began applying to all new business issued from June 29 onwards and are the result of a new agreement Fidelity Life has entered into with global reinsurer Gen Re.

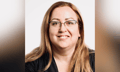

Fidelity Life chief sales and service officer Bronwyn Kirwan said she hopes advisers will welcome the new package.

“Our advisers and partners have been telling us we need to be more competitive – we’ve heard their feedback and it’s great we’ve been able to act on it,” Kirwan said. “As well as the higher non-medical limits, the removal of broad COVID-related restrictions will be of huge benefit to newly self-employed customers who don’t yet have a financial track record. This allows us to bring back income protection covers such as our New to Business and Farmers Key Person products.”

Whilst additional underwriting considerations are still necessary for new key person policies, Fidelity Life has waived blanket restrictions on customers who have been self-employed for less than three years.

According to the insurer, advisers will also benefit from simplified medical codes, making it easier to log and update customers’ medical histories in Adviser Centre.

“We’re conscious that advisers and their businesses are under pressure, including adapting to new regulations and licensing requirements, and the cost-of-living crisis,” Kirwan said. “We’re constantly looking to add value to advisers and make it easier to do business with us. We hope this package makes it just a little bit easier for advisers to help more New Zealanders get the benefits of insurance protection.”