For those who recall a time when the door was closed to the prospect of parametric insurance conversations, the changing attitude to these solutions has been an affirmation. Particularly in the wake of the LA wildfires and concerning headlines about how these are reviving ‘trauma’ for homeowners battling claims, it seems the door is opening – and swiftly – to the potential for these solutions to prove a game-changer for the insurance claims proposition.

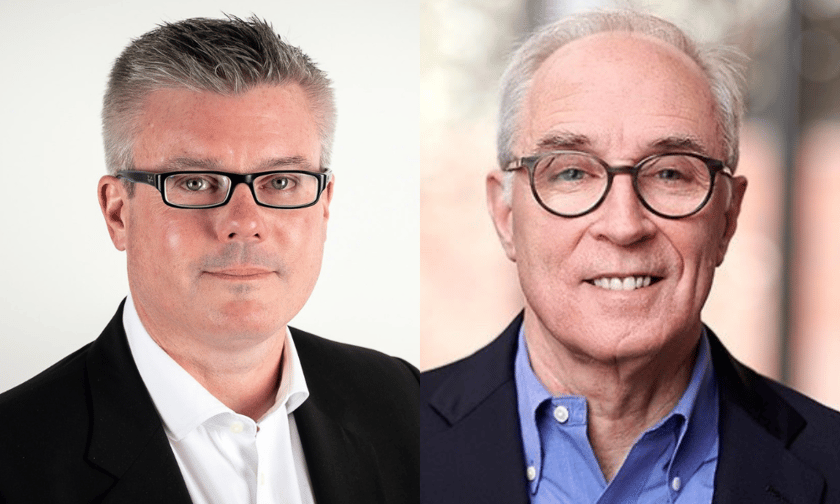

Outlining how he has seen attitudes shift “materially” since he has first had a ‘cat in a box’ product broked to him in the late noughties, Robin Ungless (pictured left), deputy CUO at Rokstone, said it has changed from what was a very niche product that was little understood to an established offering in the reinsurance product suite.

“Rather than a one size fits all prescriptive approach the product is now far more tailored to a client’s needs,” he said. “What was originally a ‘cat in a box’ can now be far more dynamic. Perils covered have broadened from wind and quake to include many others such as SCS, cyclone hail and flood.”

He highlighted that NormanMax Syndicate 3939 was the first Lloyd’s syndicate to focus on natural catastrophe parametric reinsurance products for multiple perils. Rokstone’s recent partnership with them is enabling the re/insurance MGA to now offer global parametric solutions for multiple nat cat perils.

This provides some scope to the important opportunity parametric represents for brokers to address the natural disaster protection gap created from a current lack of capacity in the nat cat market and at a time of increased climate risk and volatility. “It is flexible, responsive and provides liquidity,” he said.

“Technology too has evolved in monitoring events in a live environment, for example the introduction of Hailios which provides data on hail events. It has enabled more granular and relevant product design for buyers across the board. Buyers’ needs for cover have grown and the parametric product has grown with them.”

Bill Clark (pictured right), CEO of Demex, noted that when the firm first brought its retained climate risk reinsurance solution to the market in H1 2023, it did so in accordance with what the firm was hearing that the market needed. “We heard that from insurance brokers who were saying their clients were desperate for some kind of protection,” he said. “But everybody in the industry advised us that we were going to have a very difficult time getting capacity to support this thing.

“When we first brought it up with traditional capacity providers, some of these giant reinsurance companies quite honestly told us, ‘we have a mandate and we will not touch anything below that, because we’ve just lost too much money’.”

For Clark, changing attitudes was about connecting with the parametric desks and frequency peril desks within these large reinsurers, who were already well-versed in their own internal modeling. Having the right conversations has been key to moving the dial on parametric conversations, he said, because it means you’re talking to people who understand how you can do this business without taking on undue risk. “The answer is to be innovative with a product that works for both buyer and seller, that then bring some more safety back to the market.”

The design of parametric solutions is one that has helped move the dial on market conversations, Clark said, as a parametric resinurance offering, “they don’t face the risk of loss-cost uncertainty. Meaning, there are no claims they have to pay, it’s a modelled claims index, it’s not based on the actual claims. So, they know their maximum exposure on day one.

“And not knowing that is the big fear, that’s where they’ve gotten burned – they used to write these things on an indemnity basis and then the claims would come in, and then people would file lawsuits about the claims, or the cost of replacement was four times higher than what was factored in.”

The parametric design, he said, which provides certainty around the risk exposure, has therefore been a key factor in changing reinsurers' attitudes and making them more willing to participate in this market again.

Ungless added that material advancements in technology and enhanced data quality combined with a culture more inclined to embrace new ideas alongside traditional structures. “The alacrity of response is also key in what is a market that needs real time service,” he said.

“With the progression in the models we have turnaround times that offer the flexibility that’s so needed by buyers. When a market can continually, over time, offer speed of response, broadness of product, aligned with fast payment of claims, the proof of concept naturally changes attitudes.”