Asia Pacific’s corporate payment landscape exhibited varied trends in 2023, according to the Coface Asia Corporate Payment Survey conducted between December 2023 and March 2024.

This survey, encompassing insights from approximately 2,400 companies across nine markets in the region, provides insights into evolving payment behaviours and credit management practices.

The survey revealed a tightening of credit conditions, with a slight decrease in payment terms from 66 to 64 days compared to 2022. Concurrently, the duration of payment delays saw a marginal reduction from 67 to 65 days.

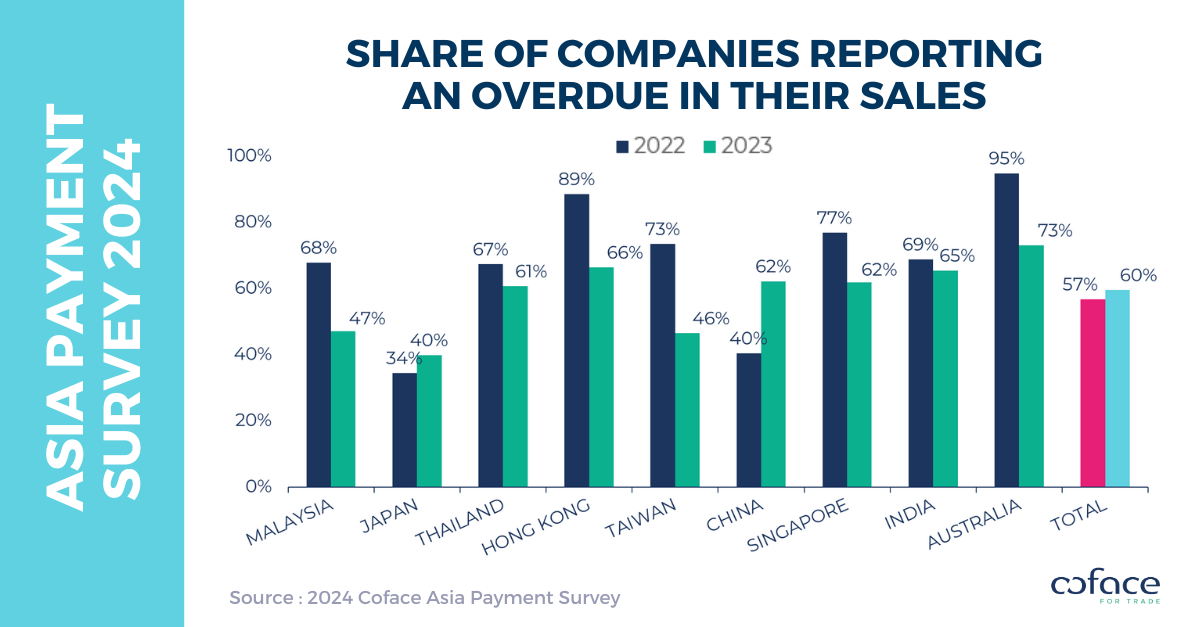

However, late payments became more prevalent, with 60% of companies experiencing them, up from 57% in the previous survey period.

Notably, the textile and construction sectors faced exacerbated payment delays, signalling challenges within these industries.

Bernard Aw, chief economist for Asia Pacific at Coface, contextualised these findings within the broader economic landscape, highlighting 2023 as a year of normalisation post-pandemic.

Concerns regarding slowing demand and intense competition resonated among respondents, underlining prevailing risks to business operations in 2024.

“The year 2023 was one of normalisation from the pandemic, but the economic landscape continued to offer its share of challenges in the form of an elevated inflationary and interest rate environment amid persistent geopolitical risks. The surveyed companies expressed the same concerns with about half of respondents citing slowing demand and over-competitive pressures as the two main risks to their company’s operations in 2024. Coface forecasts economic growth in Asia Pacific to maintain at over 4% in 2024, with the region still the fastest growing in the world,” he said.

The survey noted a rise in reported instances of payment delays, primarily driven by China and Japan due to tighter payment terms. However, other markets showcased improvements in financial stability post-pandemic, with reduced instances of payment delays reported.

Excessive competition, slowing demand, cash flow deceleration, and customer payment defaults emerged as primary reasons behind payment delays.

Textile and construction sectors bore the brunt of late payments, attributed to factors such as heightened production costs, sluggish property sectors, and elevated interest rates.

While the average duration of payment delays decreased slightly, disparities among markets were evident, with Australia, Hong Kong, and Malaysia witnessing notable increases.

Moreover, the proportion of respondents experiencing ultra-long payment delays (ULPDs) surpassed 2% of annual sales, posing significant non-payment risks.

Textile, construction, and metals sectors reported substantial shares of ULPDs, reflecting heightened vulnerability within these industries.

Despite prevailing challenges, optimism persists regarding future payment behaviours, with a notable portion of companies anticipating improvements.

Economic expectations for 2024 remain positive, with forecasts suggesting continued growth in the Asia-Pacific region, albeit amid risks such as slowing demand and competitive pressures.